Market Update June 2023

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

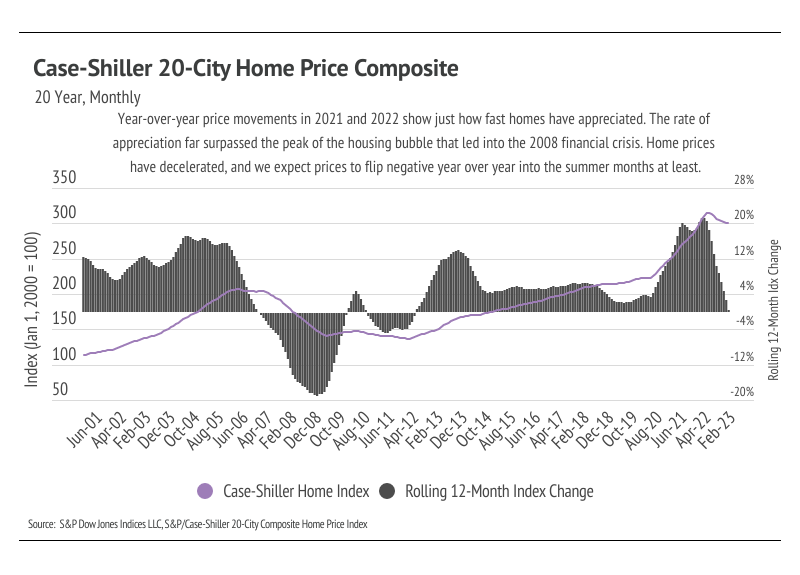

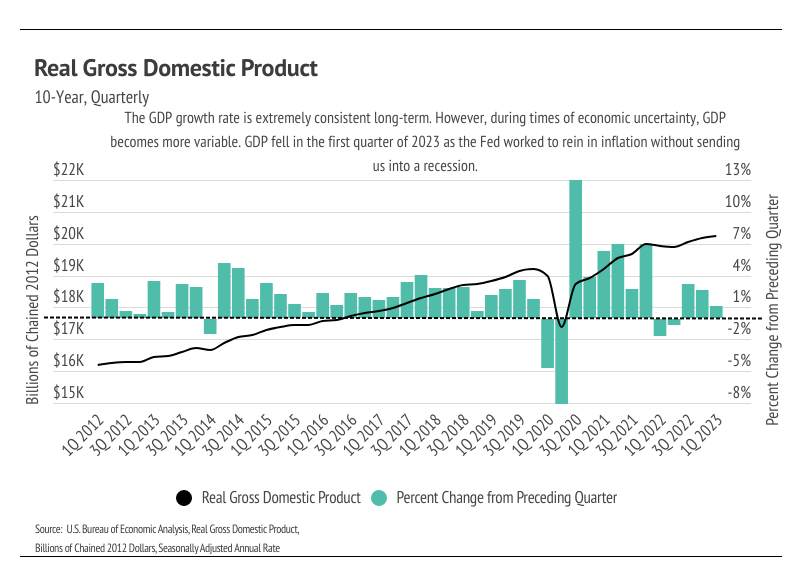

While we can say that we aren’t in a recession, it remains difficult to name the exact state of our economy. “Economic limbo” may be the right term, “uncertainty” certainly works, or “whiplash” fits. Three years post-pandemic, we are still trying to figure out the pre-pandemic economy, which grew with such stability from 2012 to 2020 that it was hard to imagine anything different. The pandemic hit and shifted our world from that of boundless, endless choice to a much smaller menu of options. Eat, work, buy, sleep, repeat. Asset prices soared. Consumers had money to spend and were eager to spend it. Easy credit conditions spurred price increases, especially home prices. The change in purchasing power in 2020 is hard to overstate. Due to falling interest rates, prices could rise 10% over the course of the year without changing the monthly cost of the mortgage. Said differently, a $500,000 loan taken in January 2020 cost the same every month as a $550,000 mortgage in December 2020. Interest rates remained consistently low in 2021.

A record number of buyers were priced into the market, and about a million more homes were sold in 2021 than the long-term average. However, skyrocketing inflation in 2021, in hindsight, was an obvious sign that the easy monetary policy was coming to a close, thereby creating the opposite effect of what happened in 2020 and 2021. The key takeaway is consumers felt wealthy and, to a large extent, were wealthier. Fewer options and opportunities to spend money led to more savings and wealth. How we feel means a lot when making big financial decisions. For many, if not most people, those feelings have changed, even if everything is technically fine on an individual level. Not that everyone (or anyone) ties their overall sense of well-being to Gross Domestic Product, an indicator of the economic health of a country or state, but recently released Q1 2023 data indicate that GDP fell from the preceding quarter, which isn’t surprising given the Fed’s effort to slow the economy. However, declining growth isn’t usually associated with rising consumer sentiments.

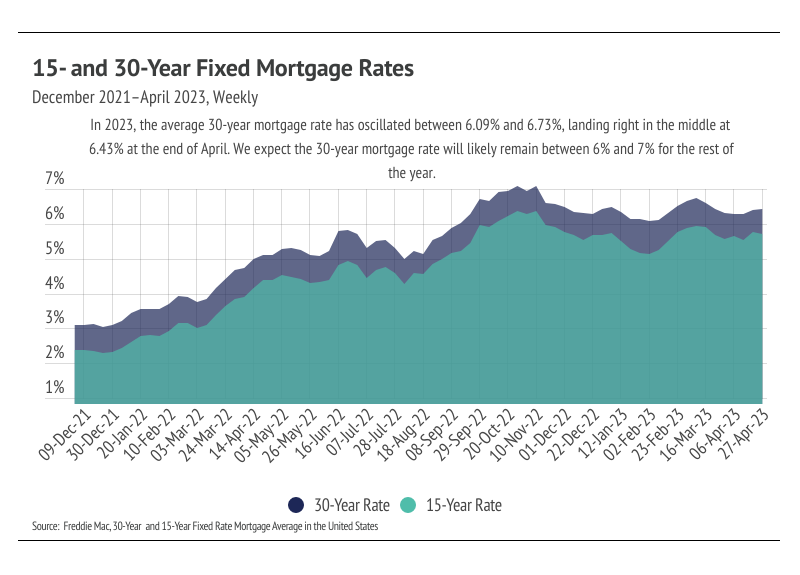

The Fed, which coincidentally met right after the March Silicon Valley Bank and Signature Bank failures, and then again right after the First Republic Bank failure in May, chose to raise their benchmark rate by 0.25% in both instances in a continuing effort to combat inflation. Banks are tightening their credit standards after the bank failures, so the Fed had less of a need to raise rates after increasing its benchmark rate 5% in the past 14 months. As the Fed assesses the impact of continued rate hikes and the fragility of the banking system, Fed Chair Jerome Powell indicated a real possibility they wouldn’t continue hiking rates this year, although there will certainly be no rate cuts. In terms of mortgage rates, we expect them to hover around 6-7% for the rest of the year.

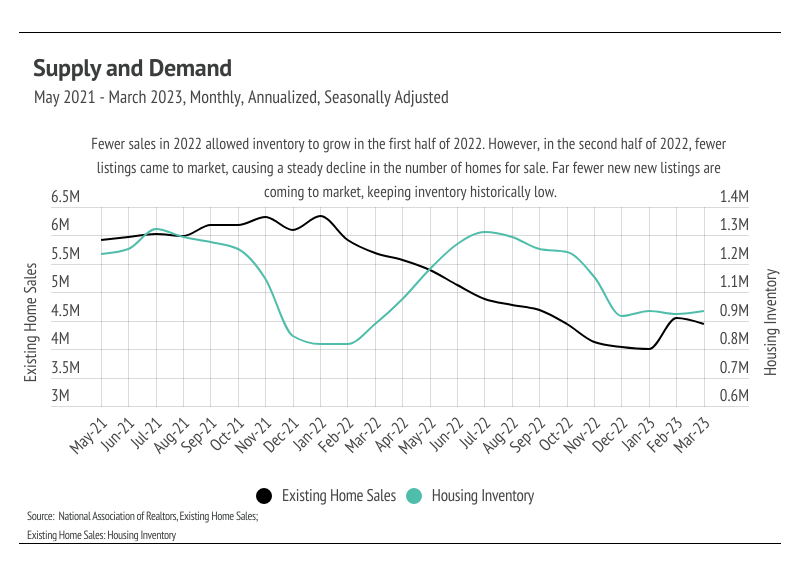

High rates coupled with high inflation negatively impacted consumer sentiment. Just as buyers were priced into the market in 2020 and 2021, they were priced out of the market in 2022. If we ignore everything except for rate increases, we would expect fewer buyers in the market. Additionally, if we have an outsized number of transactions, as we did in 2021, we would expect fewer buyers and sellers the following years because the same people don’t generally buy and sell residential property every year. Rates were so low that it was both a good time to buy and a good time to sell. Now, the housing market has to deal with both high rates and fewer market participants. Inventory is low, largely due to far fewer new listings than average coming to market. Supply of homes is low enough that, even though demand is lower on an absolute basis, it’s high relative to the number of available homes.

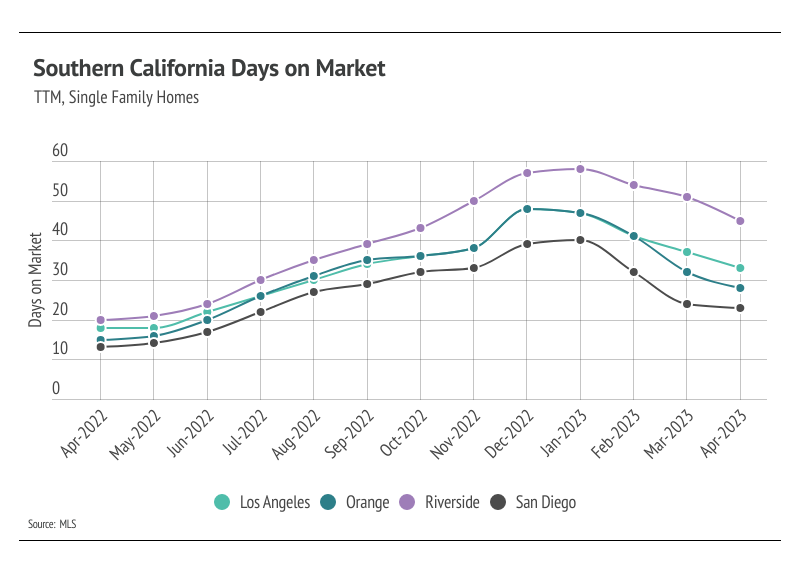

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage of your area. In general, higher-priced regions (West and Northeast) have been hit harder by mortgage rate hikes than less expensive markets (South and Midwest) due to the absolute dollar cost of the rate hikes. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Quick Take:

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

|

|

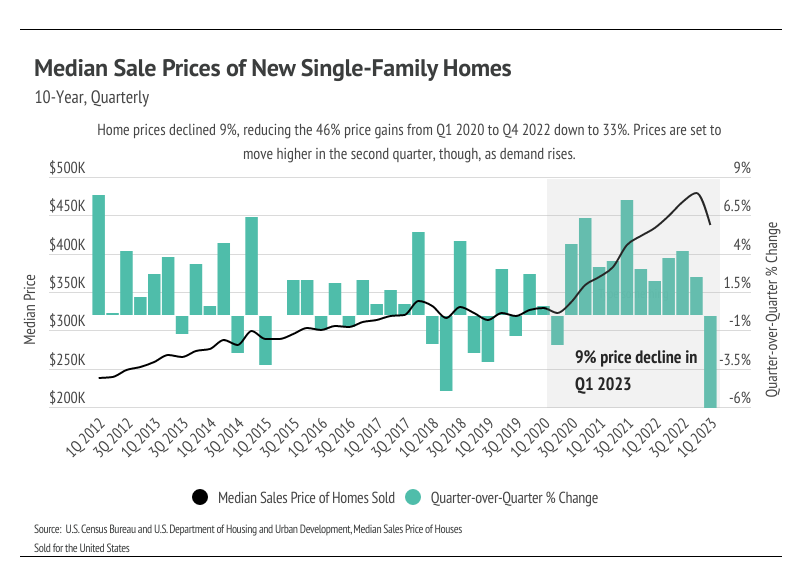

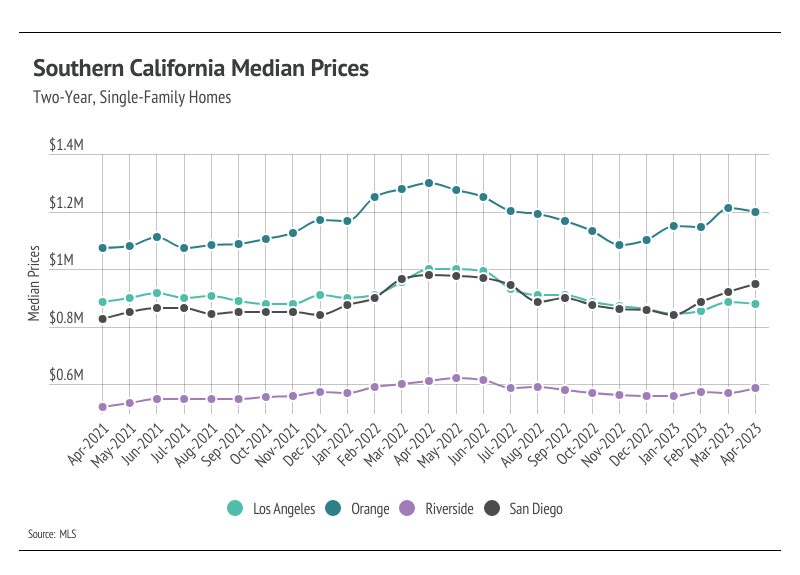

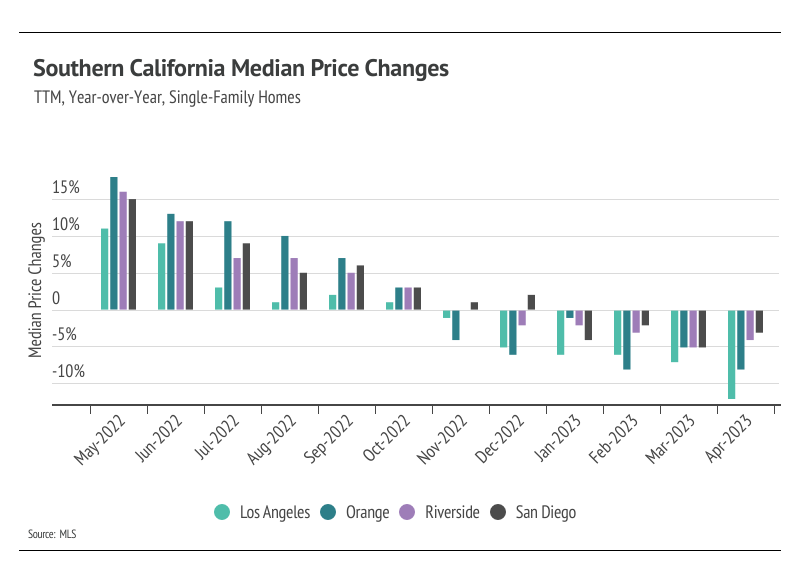

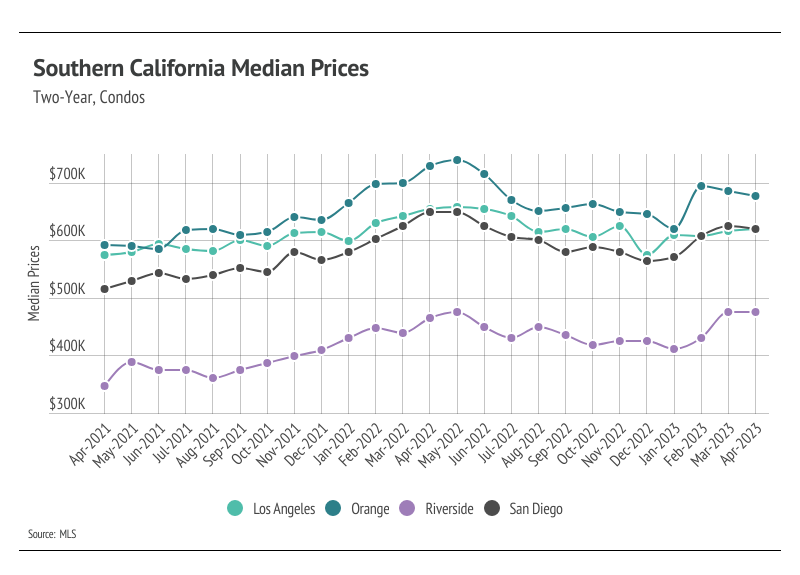

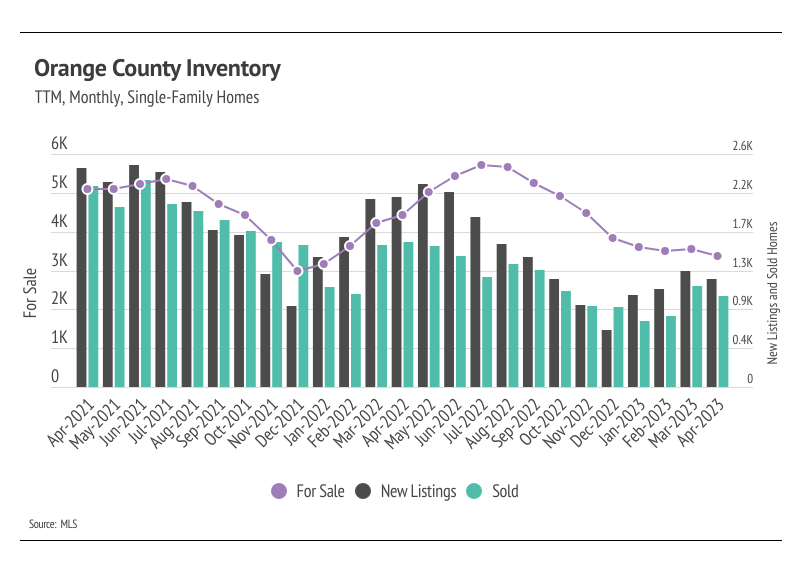

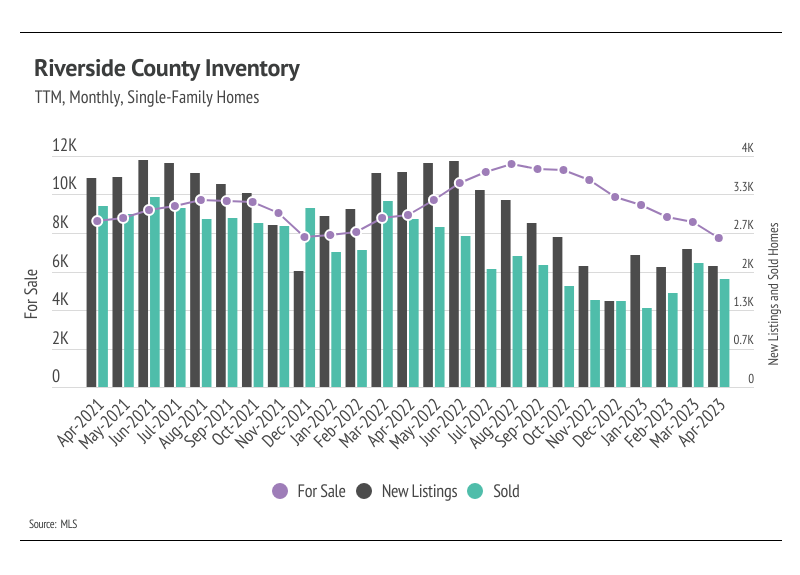

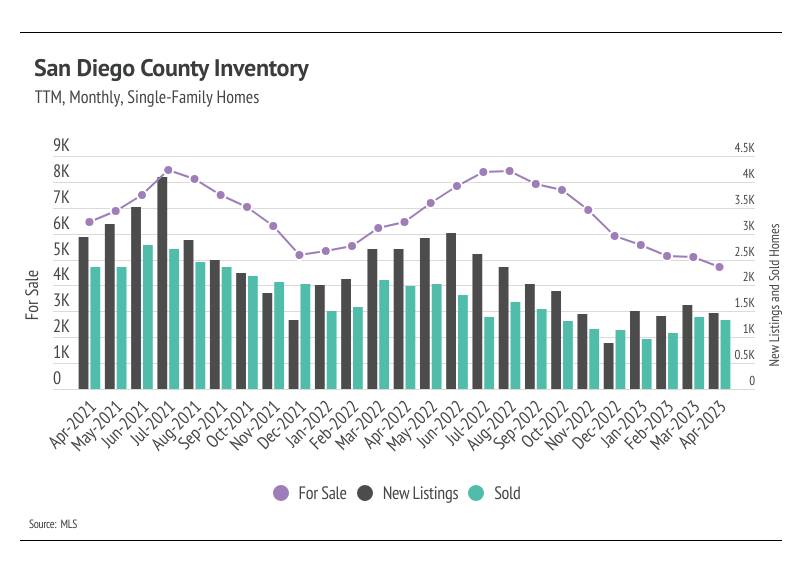

Inventory is once again driving the rapid price appreciation that Southern California is experiencing in 2023. Last year, single-family home and condo prices peaked between April and June as buyers rushed to lock in a lower mortgage rate. The Fed announced rate hikes at the end of 2021 that would swiftly affect rates in 2022. The average 30-year mortgage rate rose 2% in the first four months of 2022, crossing 5% for the first time since 2011. That 2% jump caused the monthly cost of financing to increase 27%, so buyers rightly rushed to the market. As rates rose higher, the market cooled and home prices fell in large part to accommodate the higher cost of a mortgage. Both supply and demand were lower than normal in the second half of 2022. However, in 2023, demand started to rise again despite elevated mortgage rates, but it wasn’t met with the typical number of new listings.

This year, the number of new listings has been significantly lower than usual. Typically, inventory grows in the first half of the year as new listings greatly outpace sales. At this point, inventory growth in the second quarter can’t make up for the continued inventory decline, keeping supply of homes and, in turn, sales historically low for the rest of the year. As demand increases through the summer months, competition among buyers will climb with it, raising home prices. Single-family home and condo prices are near their record highs, and if active listings drop further in the second quarter, we could easily see home prices reach new record highs by June — especially in Orange and San Diego.

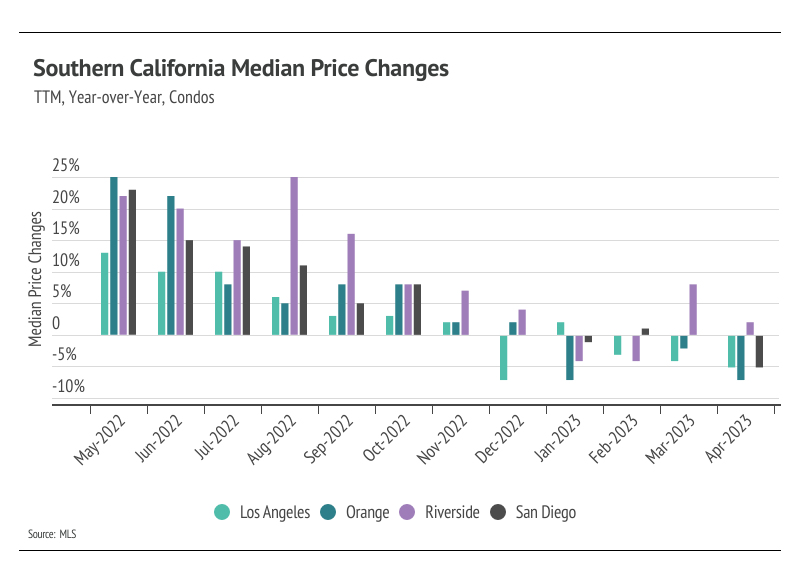

Single-family home and condo inventory has been declining for the past nine months. Total inventory, sales, and new listings all declined from March to April. However, in this instance, a decline in sales doesn’t indicate softening demand. The number of home sales is, in part, a function of the number of active listings. Sales as a proportion of active listings remained nearly the same month over month. Even with higher interest rates, which only reduces the number of potential homebuyers, seasonal demand far outpaced available inventory. Over the past three months, sales jumped 41% while new listings only increased 1%.

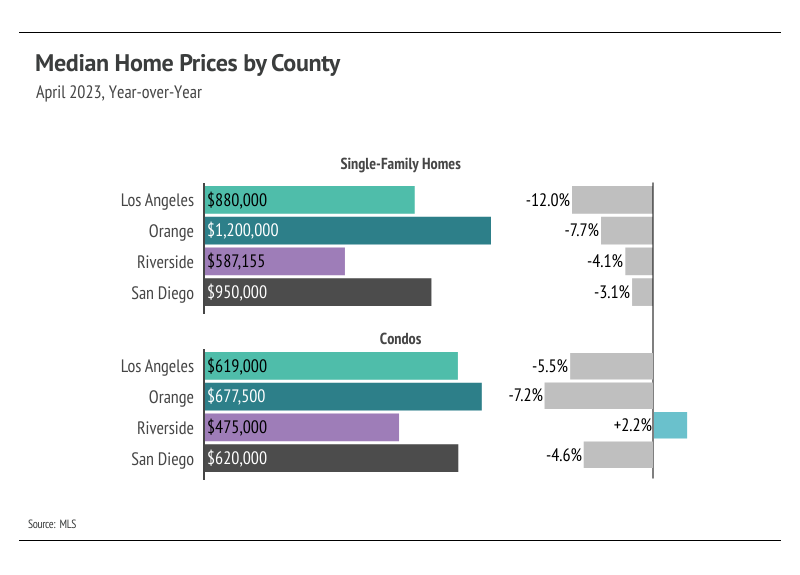

Buyer competition is certainly ramping up as inventory continues to drop, and sellers are gaining negotiating power. In January 2023, the average seller received 94% of list price compared to 98% of list in April. Inventory will almost certainly remain historically low for the year and will likely only get more competitive in the summer months.

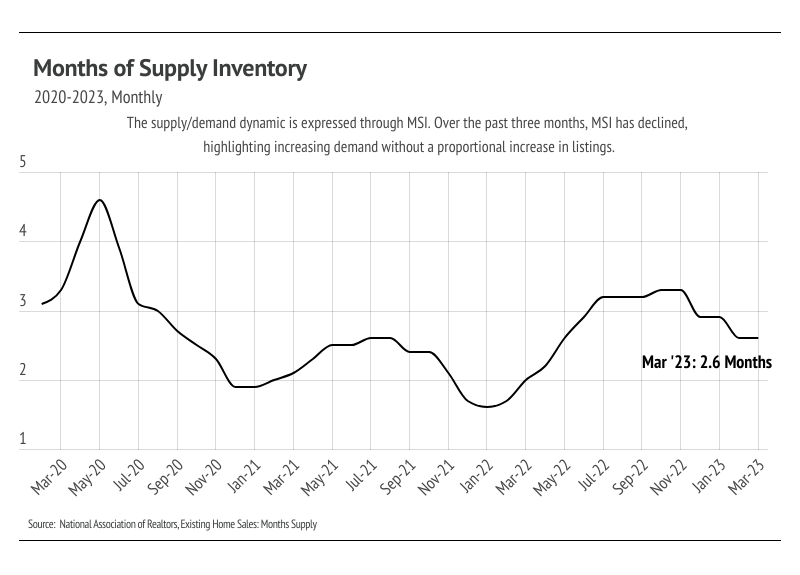

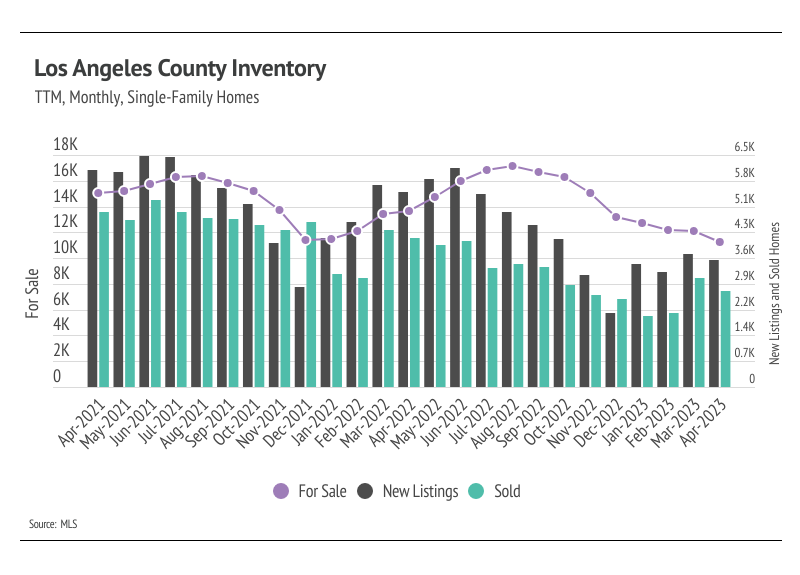

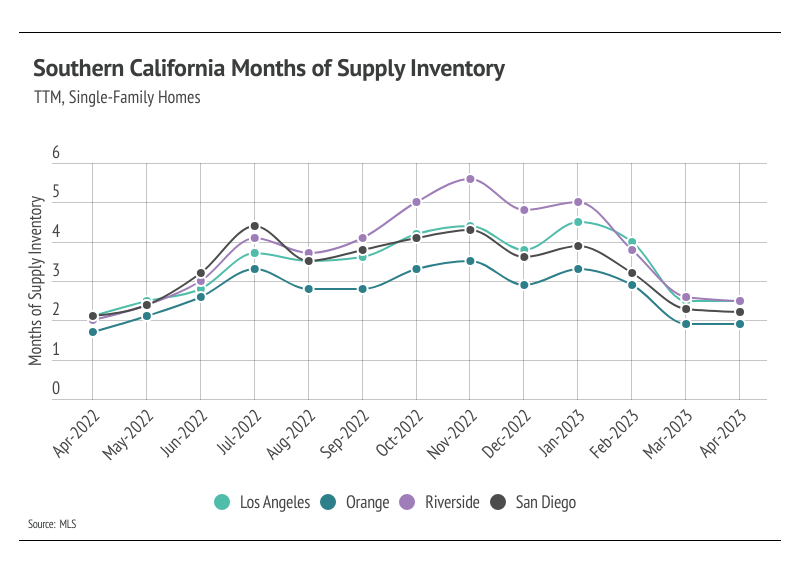

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI dropped over the past three months, dropping below three months of supply in March and declining further in April. The sharp drop in MSI occurred due to the higher proportion of sales relative to active listings and less time on the market.

Stay up to date on the latest real estate trends.

July 2026

A Closer Look at Dallas Rental Prices, Hidden Costs, and What Renters Need to Know Before Moving

June 2026

May 2026

April 2026

March 2026

February 2026

January 2026

Trusted Experts in the Palisades, Santa Monica, and Brentwood Real Estate Markets

You’ve got questions and we can’t wait to answer them.