Market Update Los Angeles

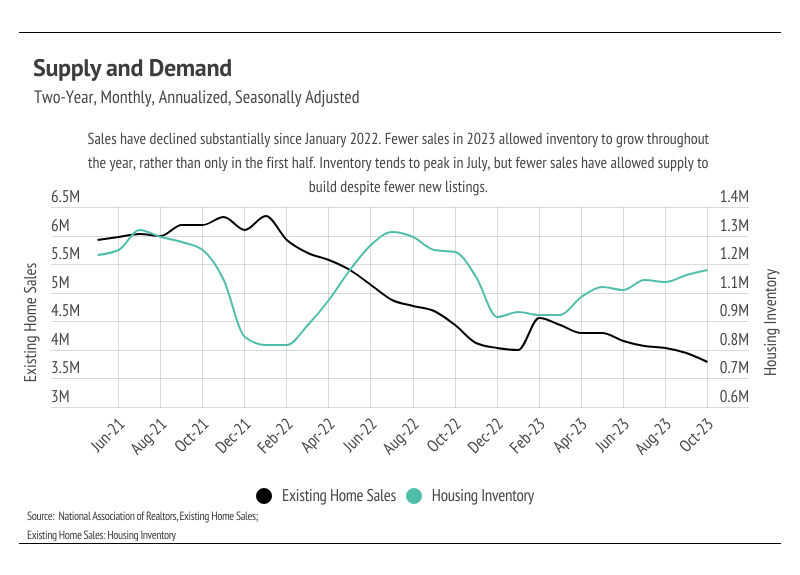

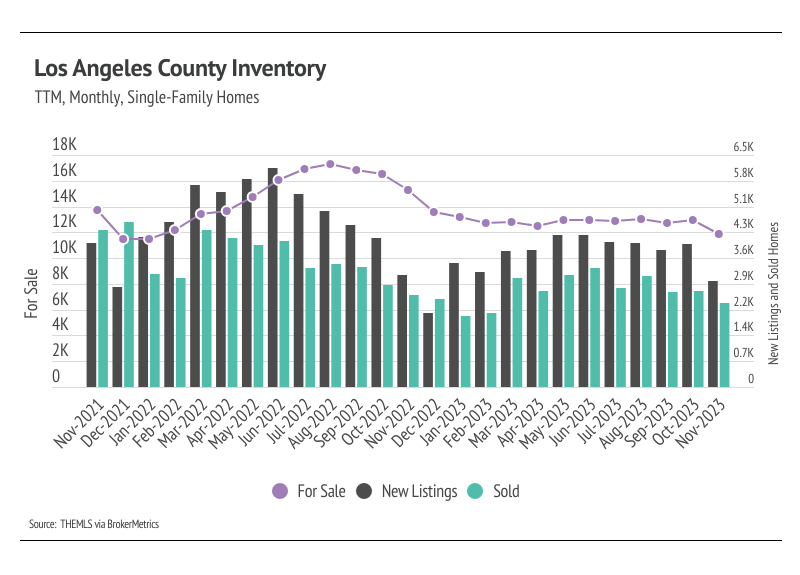

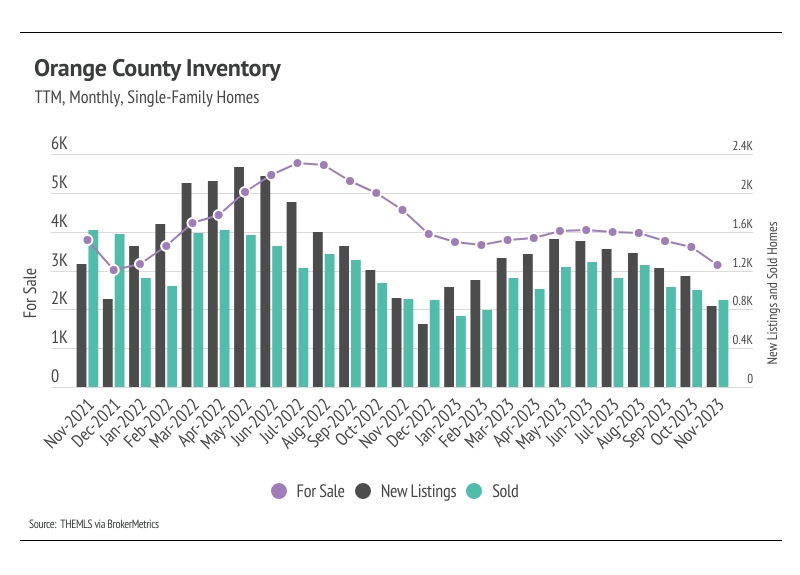

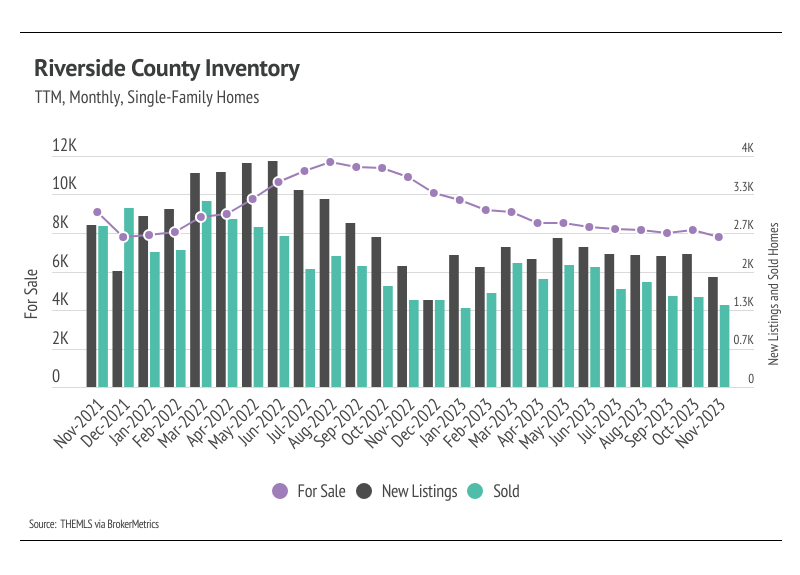

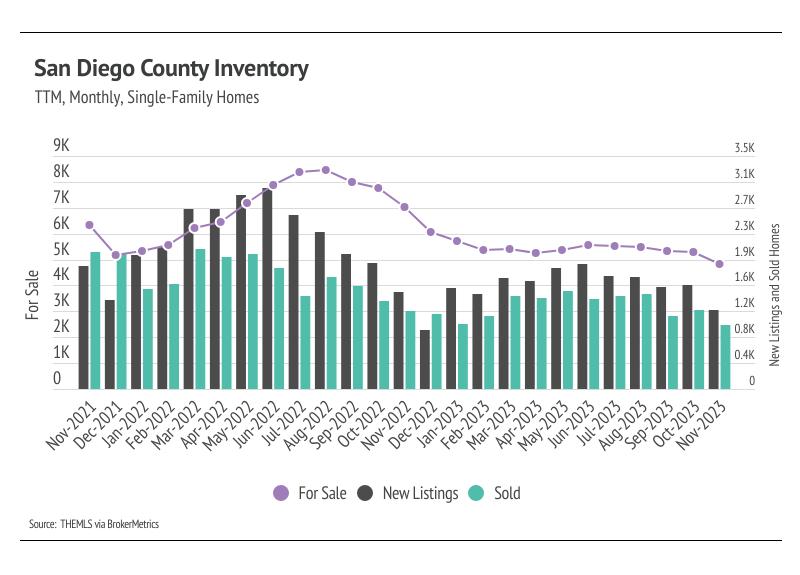

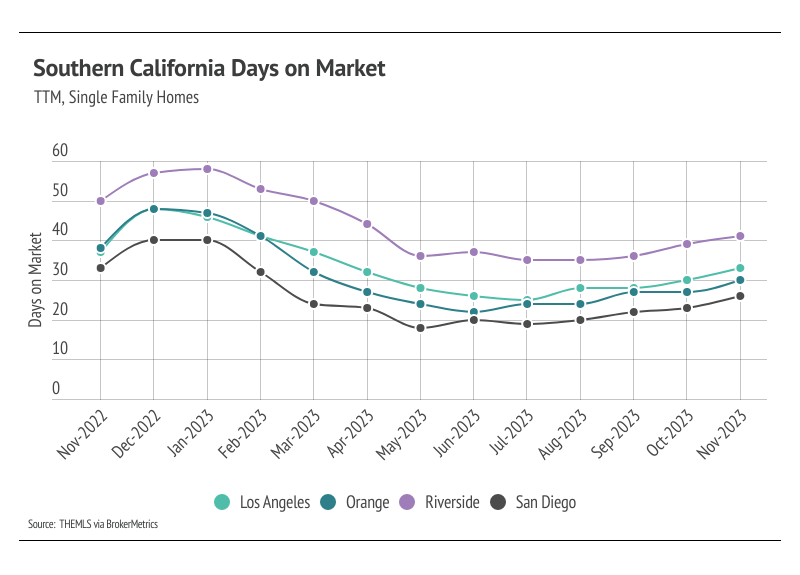

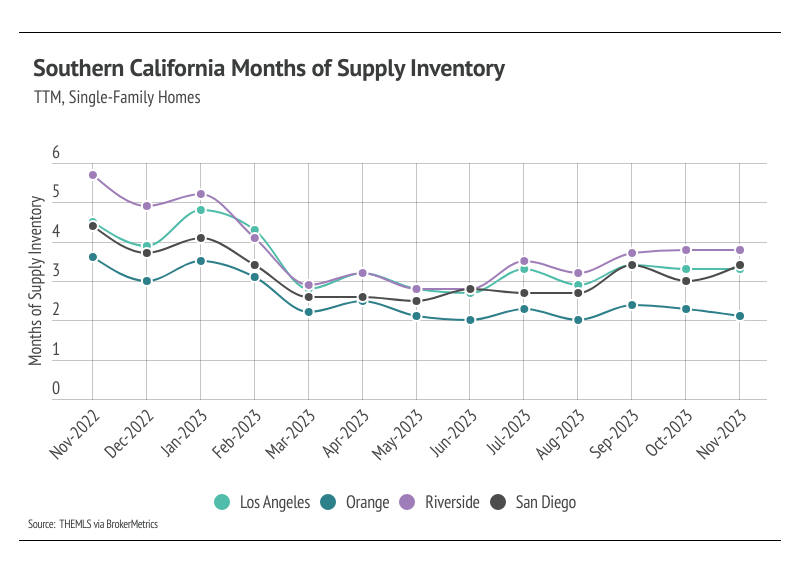

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI fell below three months in the first quarter this year and remained fairly stable from March to August. MSI jumped from August to November in Los Angeles, Riverside, and San Diego, indicating the market is more balanced for single-family homes, while Orange County MSI fell, implying that market still favors sellers.

Stay up to date on the latest real estate trends.

July 2026

A Closer Look at Dallas Rental Prices, Hidden Costs, and What Renters Need to Know Before Moving

June 2026

May 2026

April 2026

March 2026

February 2026

January 2026

Trusted Experts in the Palisades, Santa Monica, and Brentwood Real Estate Markets

You’ve got questions and we can’t wait to answer them.