Market Update Dallas

Note: You can find the charts & graphs for the Big Story at the end of the following section.

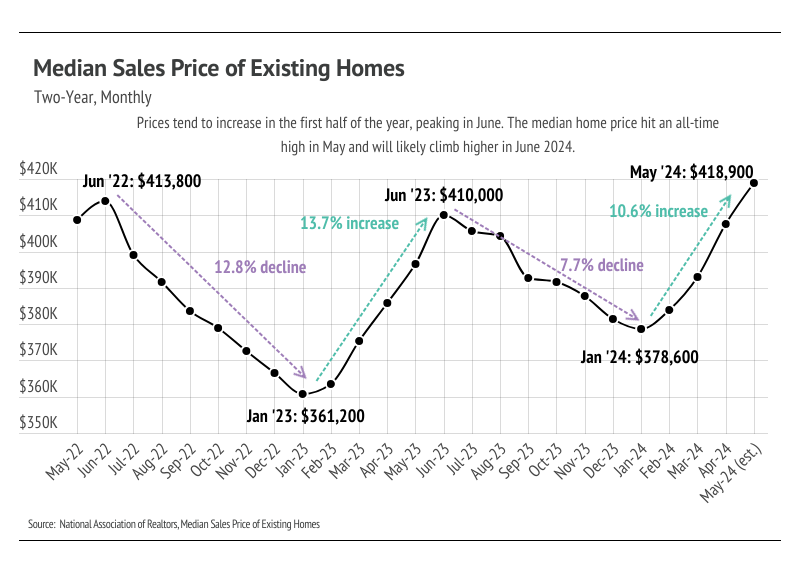

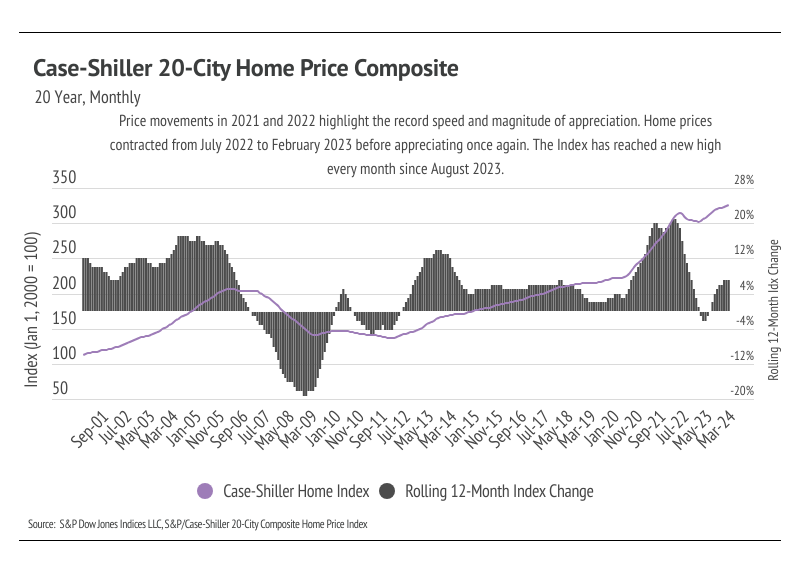

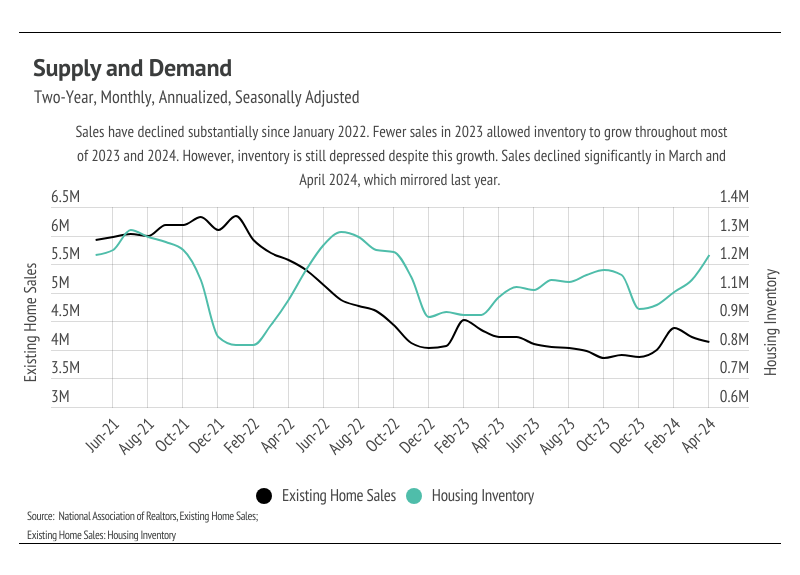

According to the National Association of Realtors® (NAR), the median sales price for existing homes grew 5.6% to $418,900 between May 2023 and the present — the eleventh consecutive month of year-over-year price growth, and the highest median price ever reached. Typically, the median price peaks in June each year, so we will likely see prices climb even higher when the data comes in for this month. In addition to NAR, the Case-Shiller 20-City Composite Home Price Index, which measures the aggregate price level of homes in the largest 20 metropolitan statistical areas, has reached a new high for the eighth month in a row. The combination of elevated mortgage rates and rising prices has brought affordability to an all-time low, which translates to fewer sales and growing inventory. However, at the same time, homes are spending less and less time on the market.

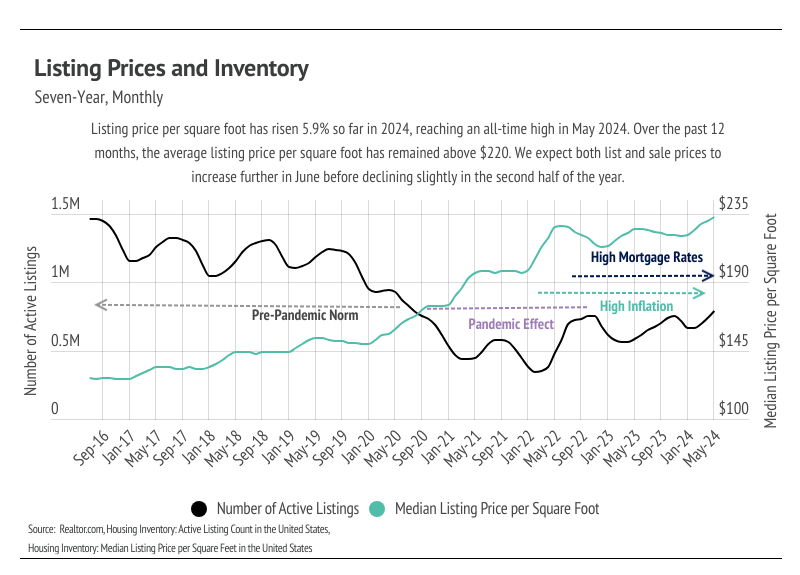

Demand is still high relative to supply, even though inventory is building. The buyers that haven’t been priced out of the market are moving quickly on homes that suit them. Despite the high demand and quick market, there are simply fewer buyers in the market. Higher mortgage rates can only lead to fewer market participants. On the bright side, inventory growth is great news for the wildly undersupplied U.S. housing market. According to data from realtor.com, inventory reached its highest level since August 2020. The market is still broadly undersupplied, but the increasing inventory level should cause rising home prices to slow. Decreasing home prices mid-year is also normal on a seasonal basis. In the pre-pandemic seasonal trends, sales, new listings, inventory, and price would roughly all rise in the first half of the year and decline slightly in the second half of the year. Sales and new listings have been far lower than usual since mortgage rates started climbing, which is to be expected.

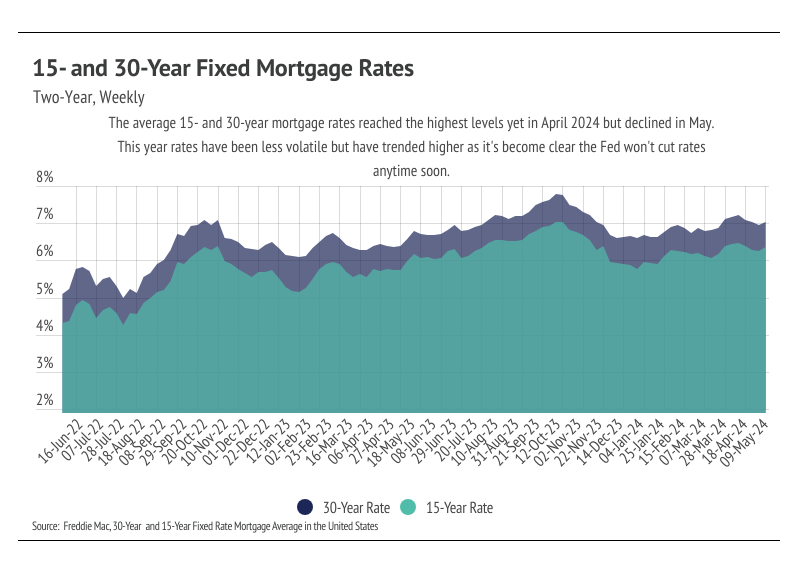

The average 30-year mortgage rate began the year at 6.62% and landed at 7.03% at the end of May, marking the third year mortgage rates have been elevated. At the start of the year, rate expectations were far different from those today. In January, inflation still appeared to be trending lower, and economists were predicting rate cuts as early as March. However, in hindsight, inflation stopped trending lower in June 2023 and has held fairly steady around 3.3% since then. The Fed targets an inflation rate of 2%, so we aren’t expecting rate cuts anytime soon. In fact, the safest bet may be to not expect any rate cuts in 2024. The Fed’s dual mandate aims for stable prices (inflation ~2%) and low unemployment, so it’s all about inflation, especially because the job market is still strong.

During the Fed’s May meeting, the Federal Reserve Board unanimously voted to hold policy rates steady for the sixth consecutive time, leaving the federal funds target rate unchanged at 5.25% to 5.50%. Although this letter was written before the June 11-12 Fed meeting, we are confident the Fed will hold rates steady. If there’s a silver lining, it’s that even though rate cuts are extremely unlikely, rate hikes are even less probable.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

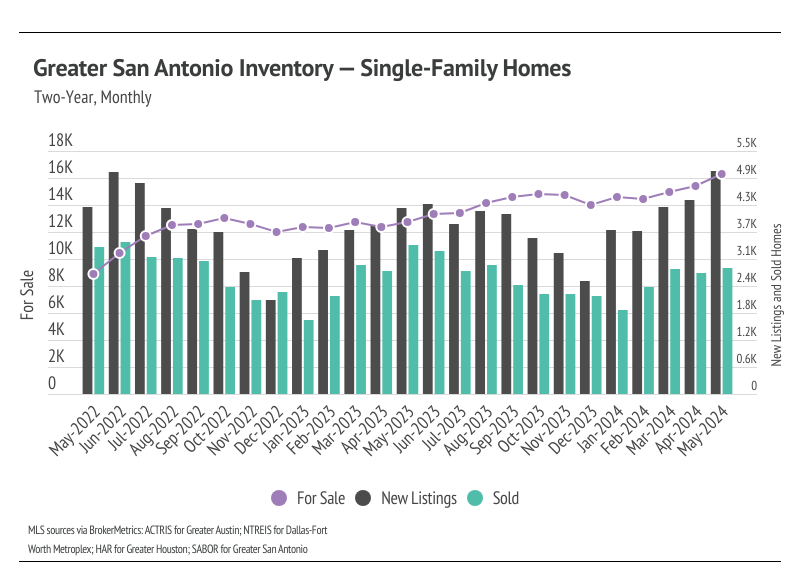

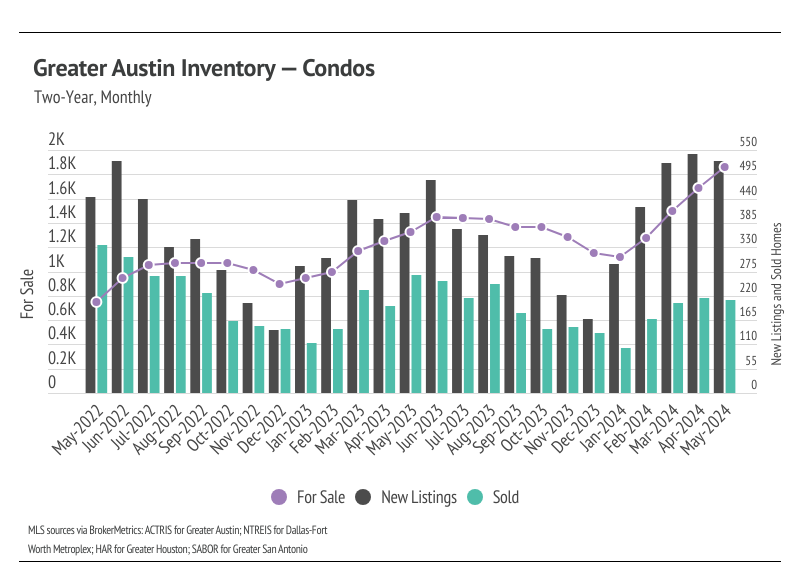

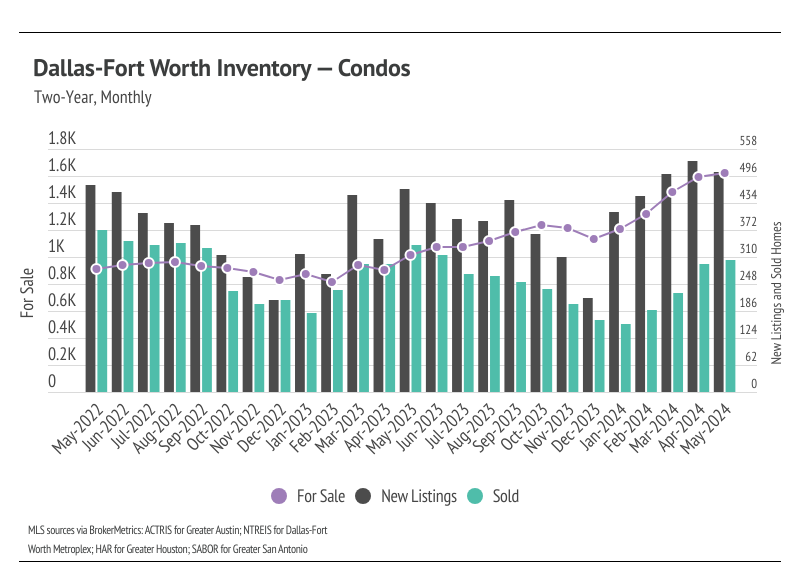

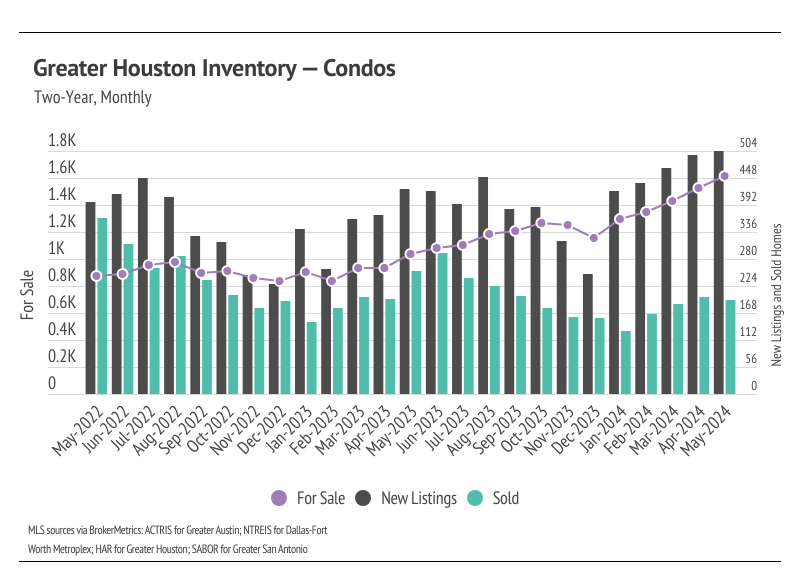

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

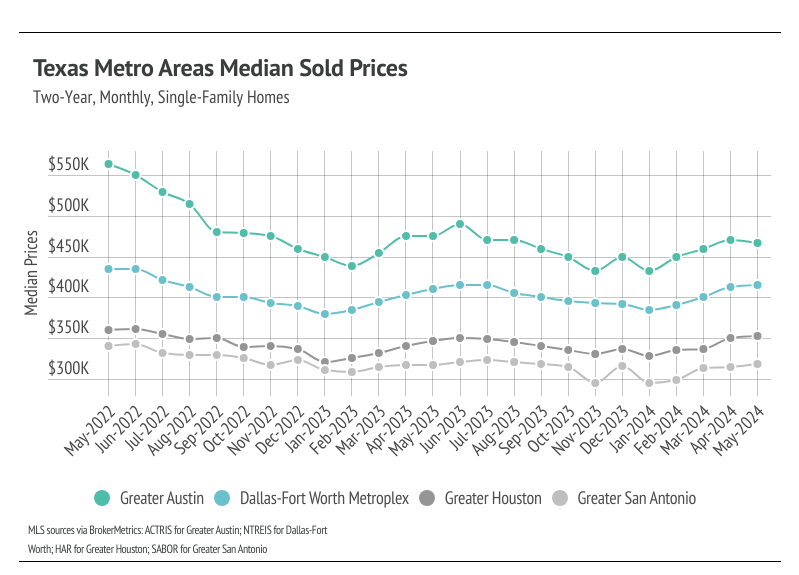

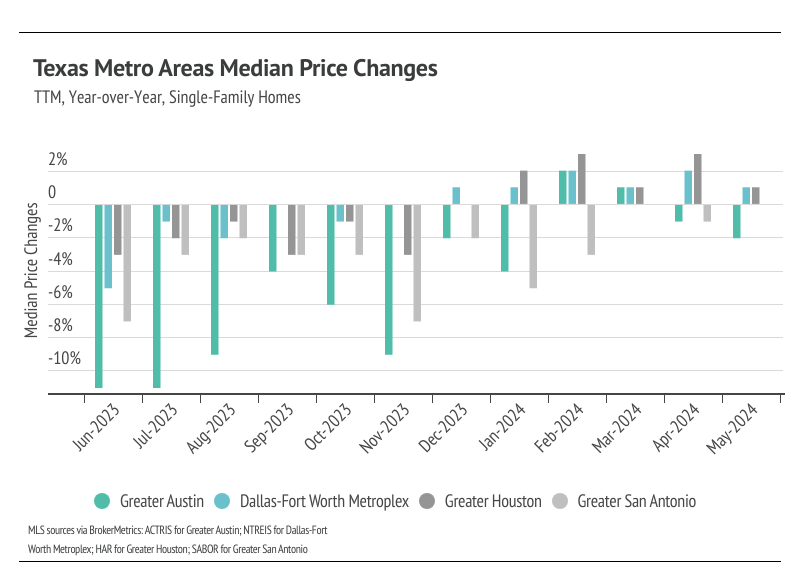

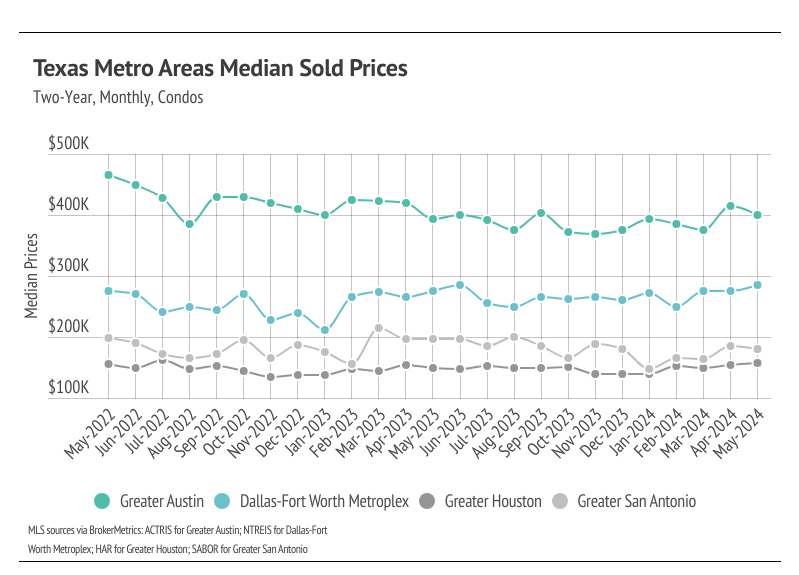

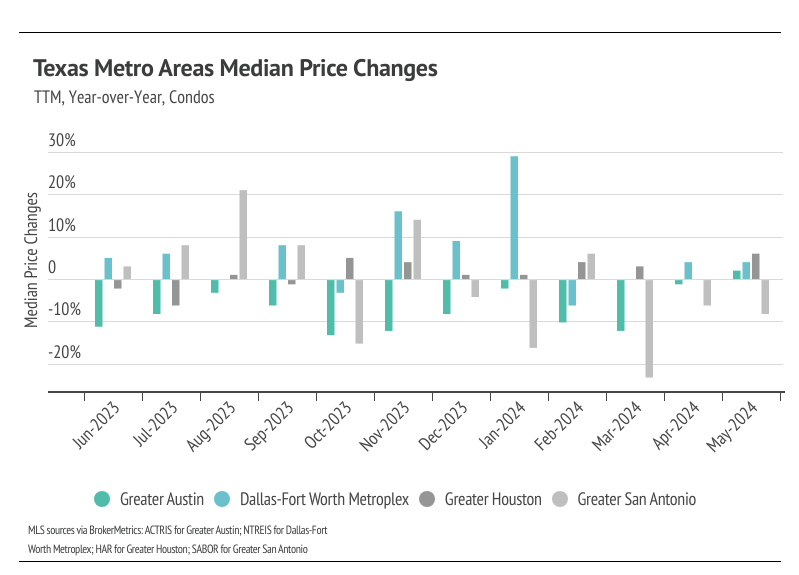

In Texas, home prices haven’t been largely affected by rising mortgage rates with the exception of Greater Austin, which has had a major price contraction since May 2022. Broadly, price contractions are normal in the fall and winter months of any year, so it’s hard to conclude that higher rates had any meaningful effect on price across most of Texas’ major metros. We expected prices to remain below peak in the winter, but as seasonal demand increased in the spring, prices started to increase. However, we don’t expect record high prices in the summer months. The inventory buildup in 2023 has created a healthier market in 2024, satiating demand as it has grown. We expect single-family home prices to continue to rise next month, as the rising inventory and new listings attract more buyers to the market.

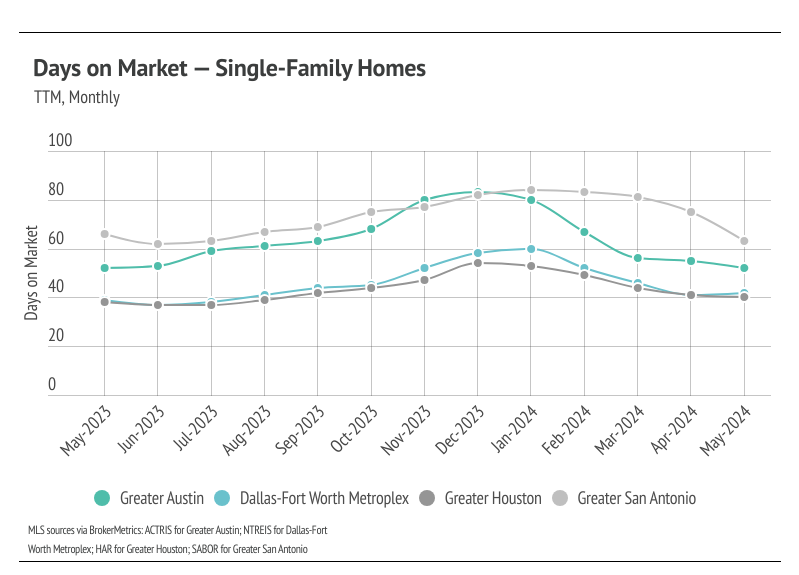

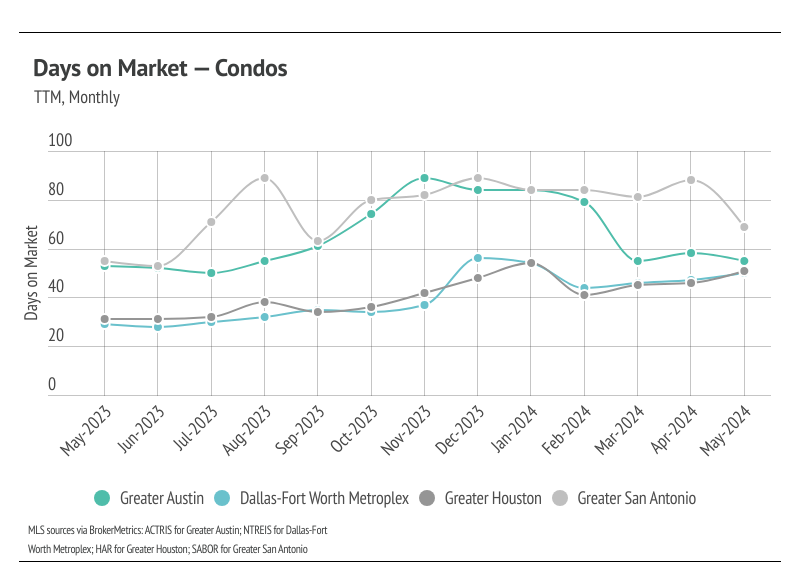

High mortgage rates soften both supply and demand, but home buyers and sellers seemed to tolerate rates above 6%. Now that rates are above 7%, sales could slow once again during the time of the year when sales tend to be at their highest. This phenomenon wouldn’t be great for the market, but it wouldn’t be terrible, either, as it may allow inventory to build further.

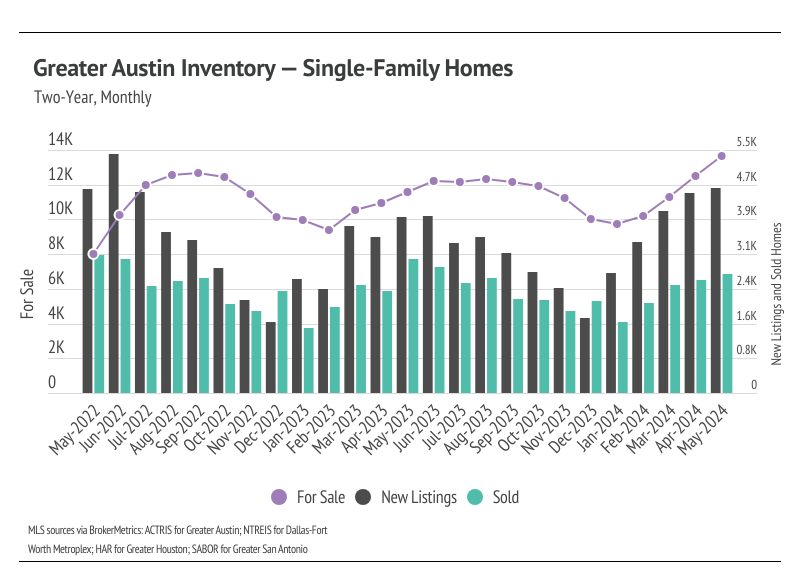

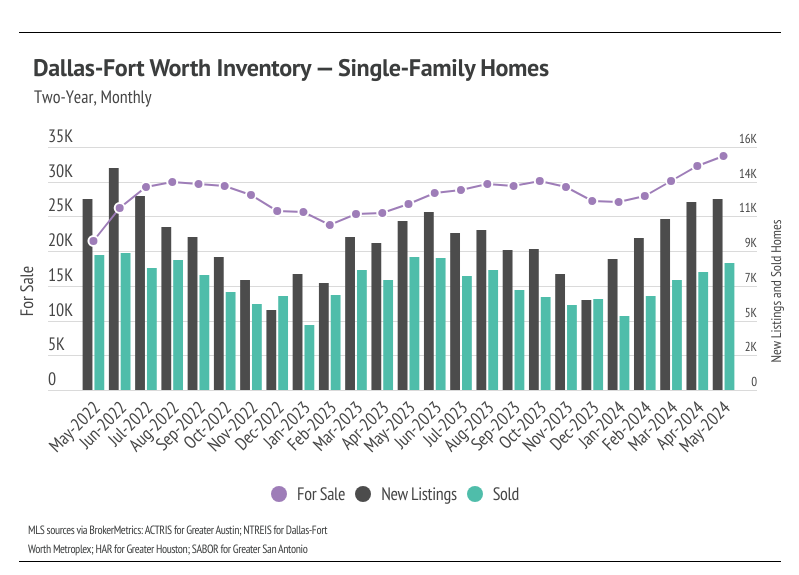

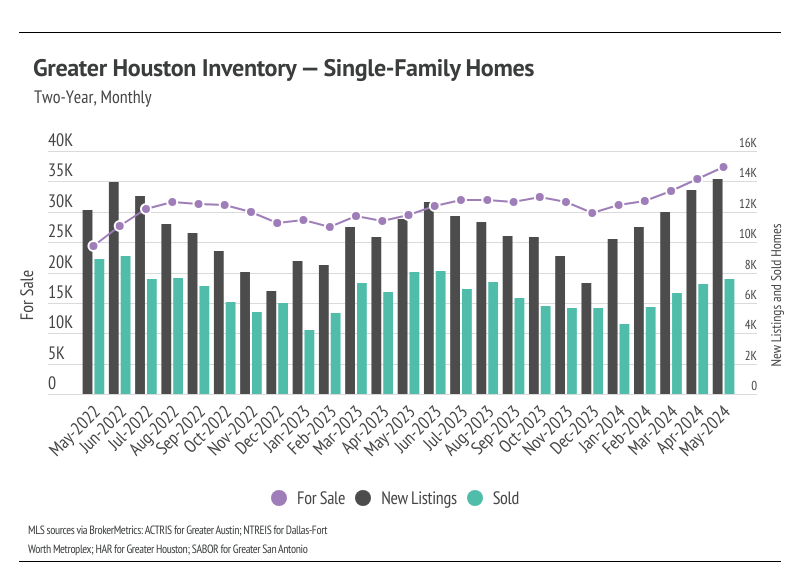

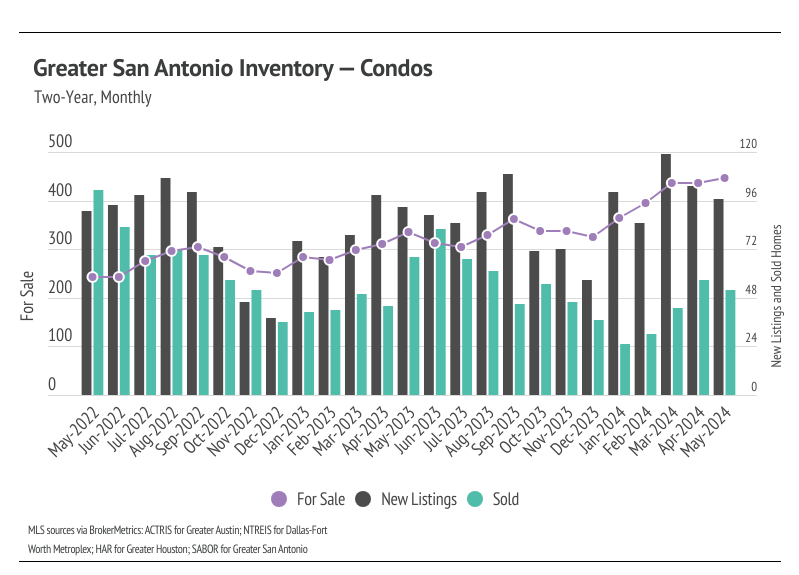

Inventory trended higher into the fall of 2023 and winter 2023/2024, which is far from the seasonal norm. Typically, inventory peaks in July or August and declines through December or January. Inventory levels in Texas’ major metro areas are unusual in the United States, in that they actually built up to pre-pandemic levels in 2023, moving higher primarily due to softening demand caused by higher interest rates.

During Q4 2023, inventory peaked in October before declining slightly in November and December, as sales and new listings declined. In 2024, inventory has begun to increase once again. Notably, inventory across markets reached a two-year high in May. The number of new listings coming to market is a significant predictor of sales, and the substantial increase in new listings so far in 2024 has led to an increase in sales month over month. The next three months will determine if the higher mortgage rates will actually slow the market, but so far, rates haven’t hurt sales.

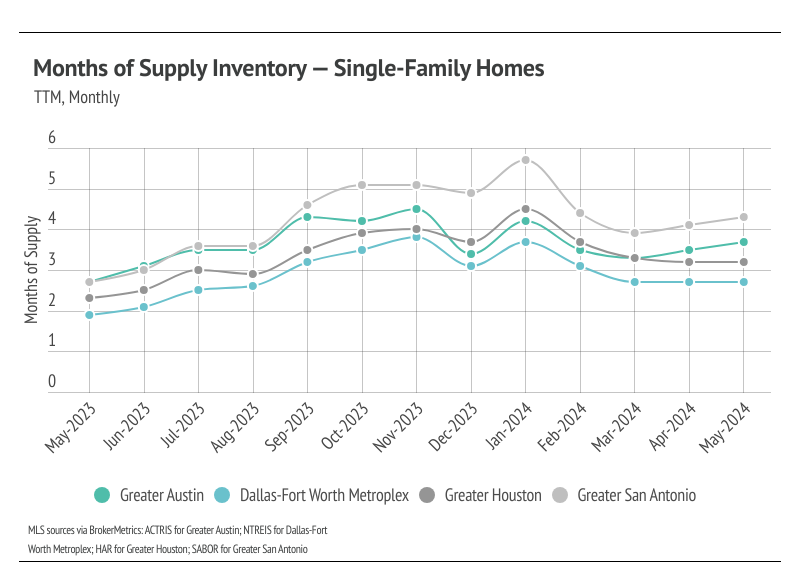

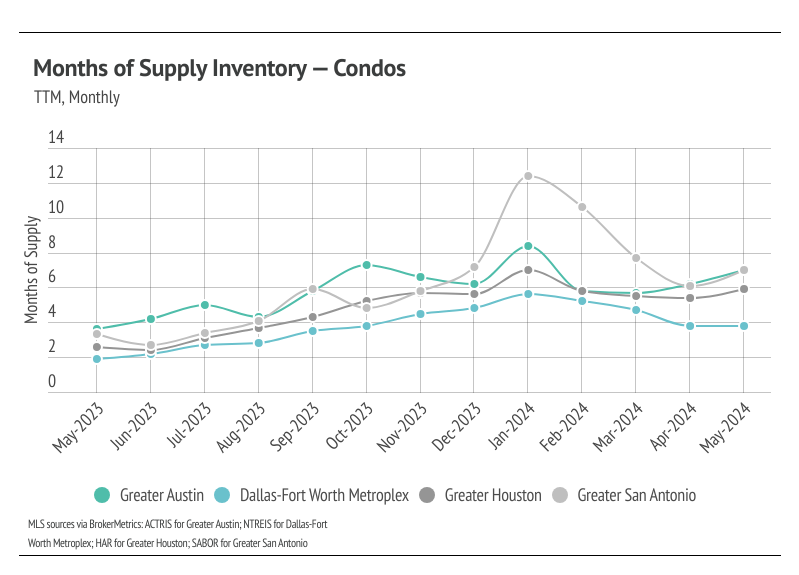

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around four to five months in Texas, which indicates a balanced market. An MSI lower than four indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while an MSI higher than five indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI trended higher from May 2023 to January 2024 largely due to the decline in sales and longer time on the market. However, in February and March 2024, MSI declined across markets as sales rose and homes sold at a faster rate. April MSI movements were mixed in Texas markets, and in May, MSI rose across markets. Currently, for single-family homes, MSI indicates that Greater San Antonio is balanced, while Greater Austin, Greater Houston, and Dallas-Fort Worth favor sellers. For condos, MSI indicates that the markets favor buyers except for Dallas-Fort Worth, which now favors sellers.

Stay up to date on the latest real estate trends.

May 2026

April 2026

March 2026

February 2026

January 2026

Trusted Experts in the Palisades, Santa Monica, and Brentwood Real Estate Markets

How Sellers In Pacific Palisades, Santa Monica And Brentwood Get It Right

December 2025

November 2025

You’ve got questions and we can’t wait to answer them.