Market Update Dallas

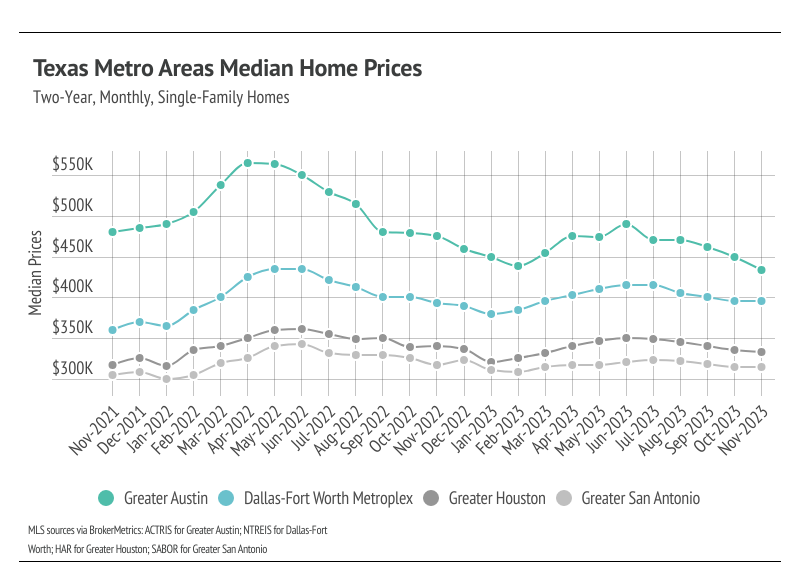

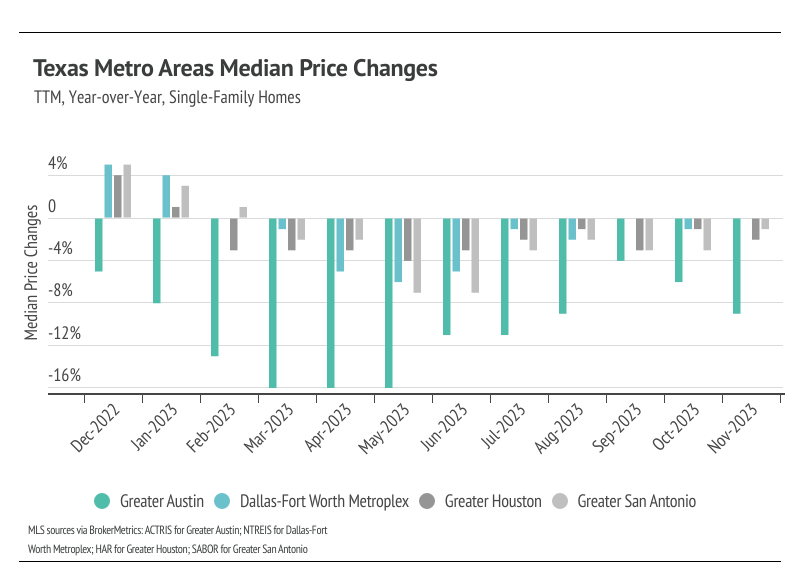

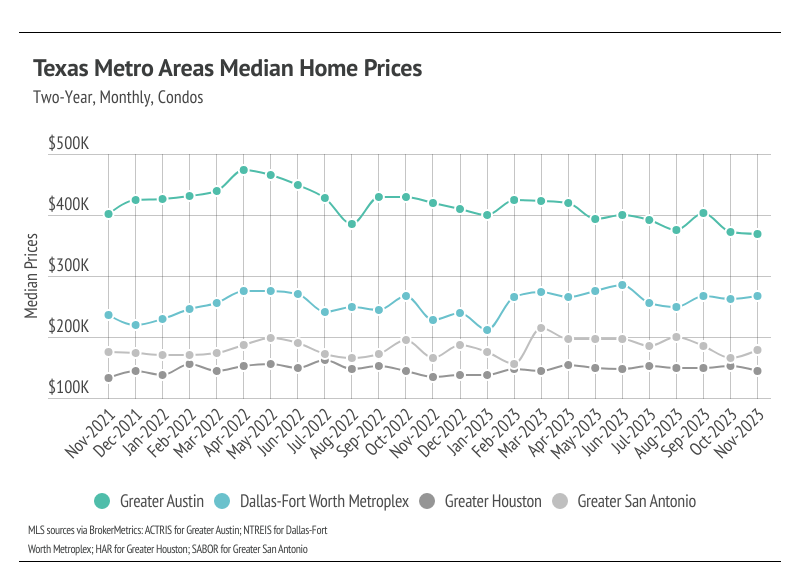

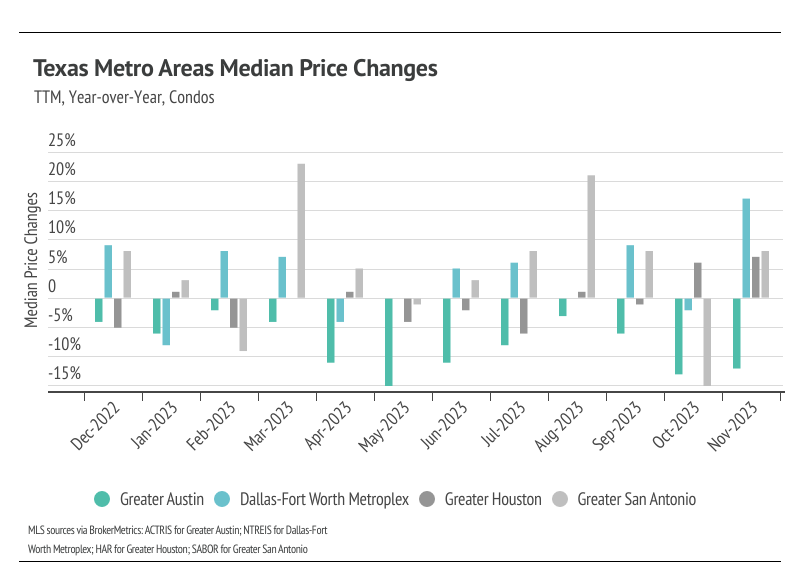

In Texas, the home prices haven’t been largely affected by rising mortgage rates with the exception of Greater Austin, which has had a major price contraction since May 2022. Broadly, price contractions are normal in the second half of the year, so it’s hard to conclude that higher rates have had any meaningful effect on price across most of Texas’s major metros. We expect prices to remain below peak in the winter months, but as interest rates decline, prices will almost certainly reach new highs in the first half of 2024 in all the selected major markets except Greater Austin. Additionally, the inventory build-up in 2023 will create a healthier market in 2024, satiating demand as it grows.

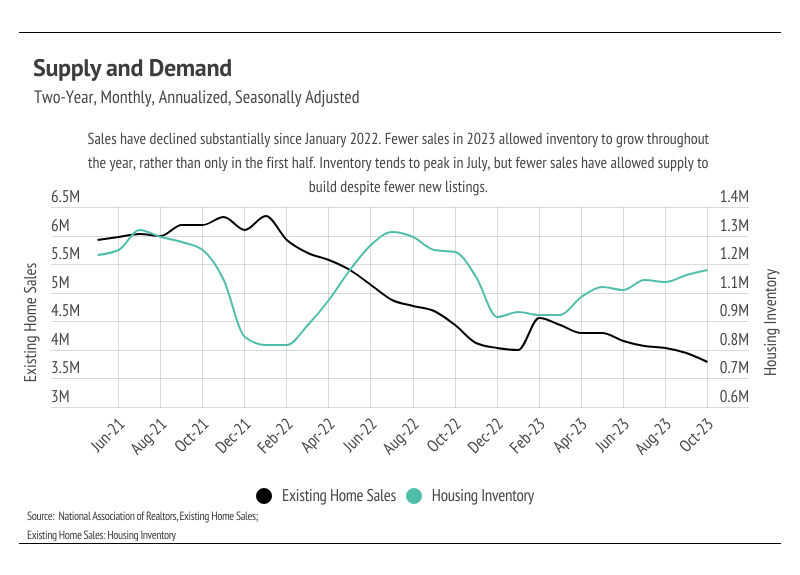

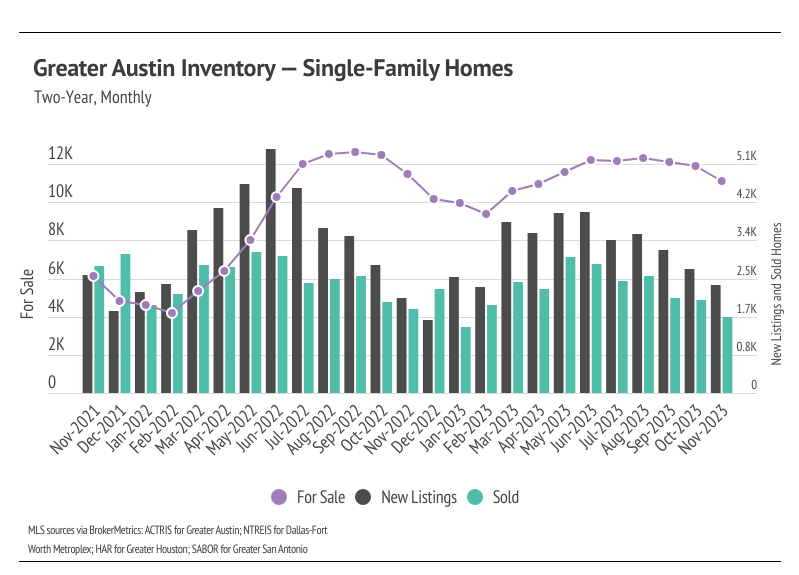

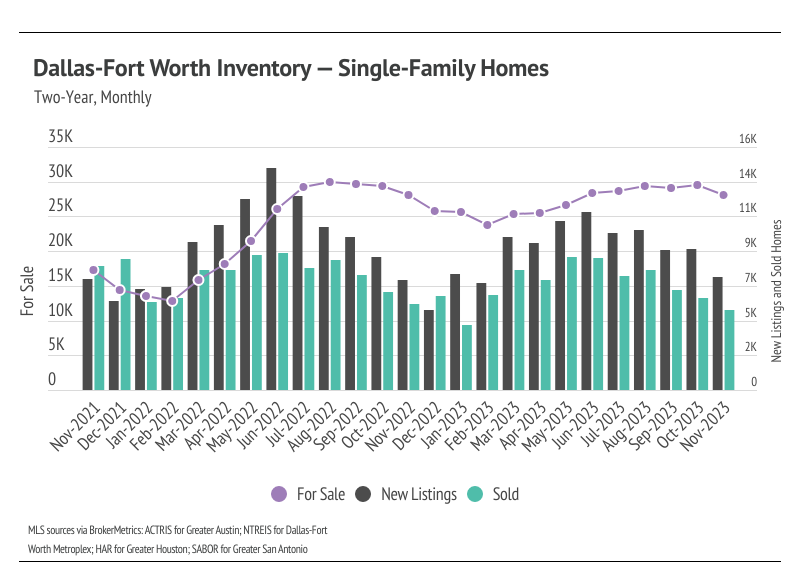

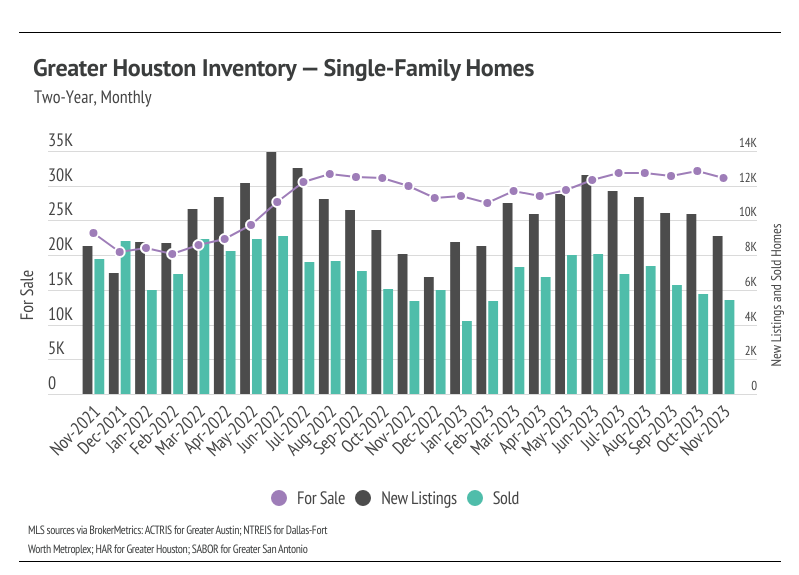

High mortgage rates soften both supply and demand, so ideally, as rates fall, far more sellers will come to the market. Rising demand can only do so much for the market if there isn’t supply to meet it. Unlike 2023, 2024 inventory has a much better chance of following more typical seasonal patterns.

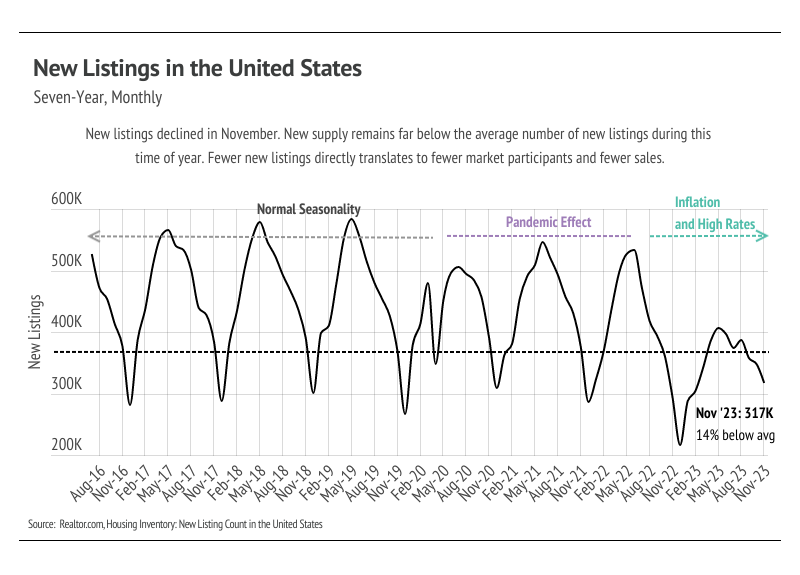

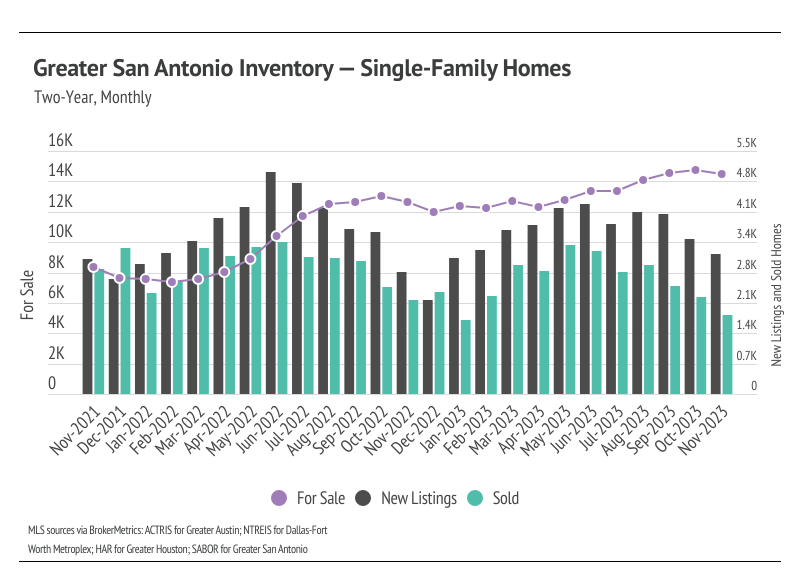

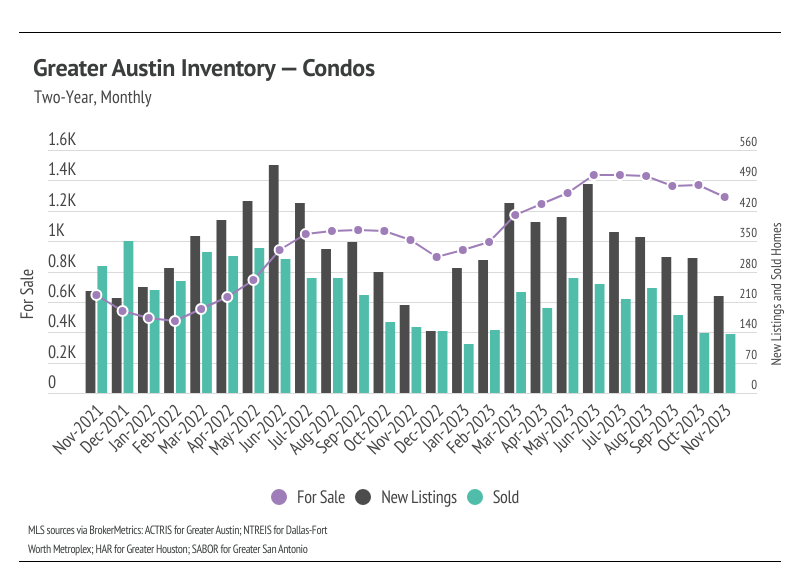

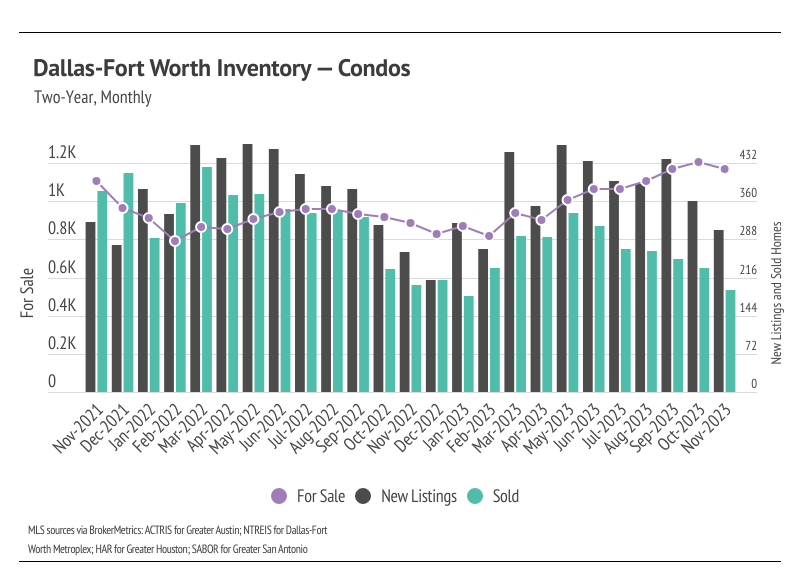

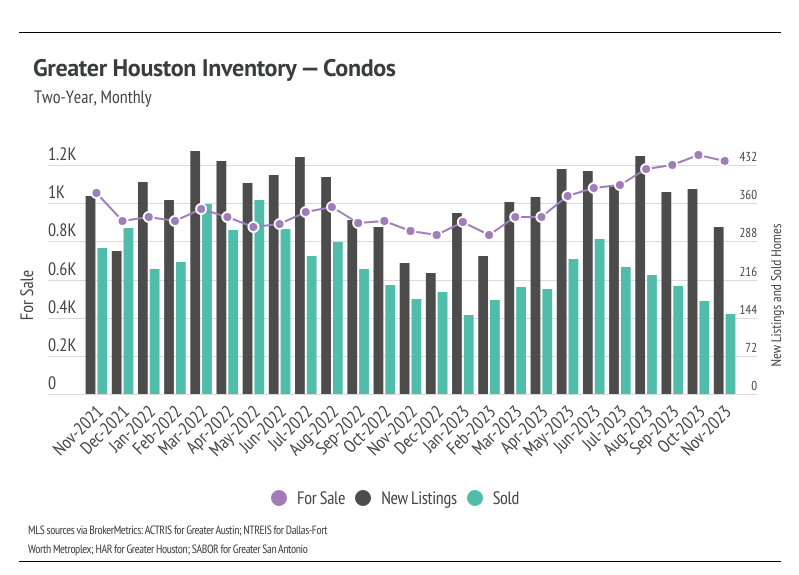

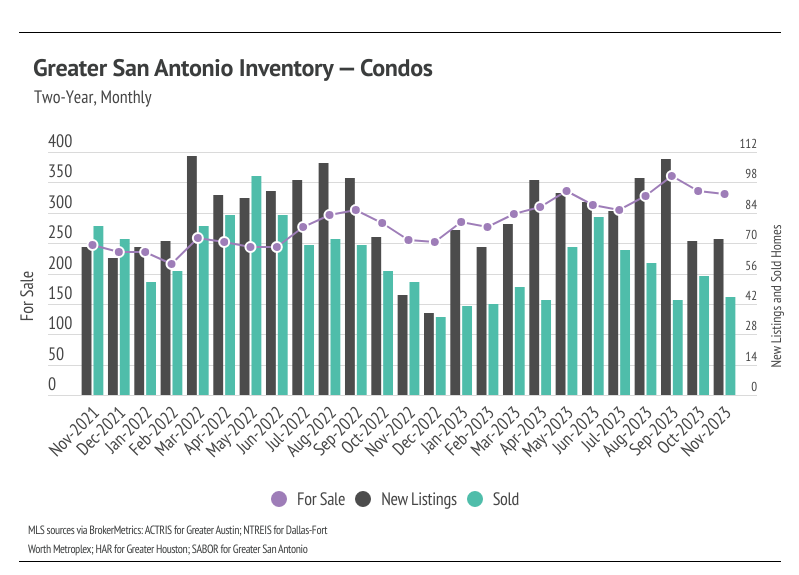

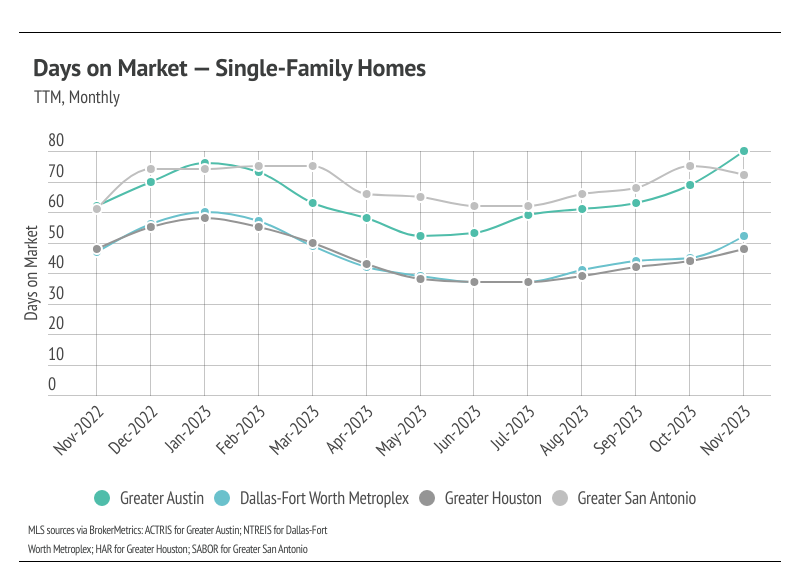

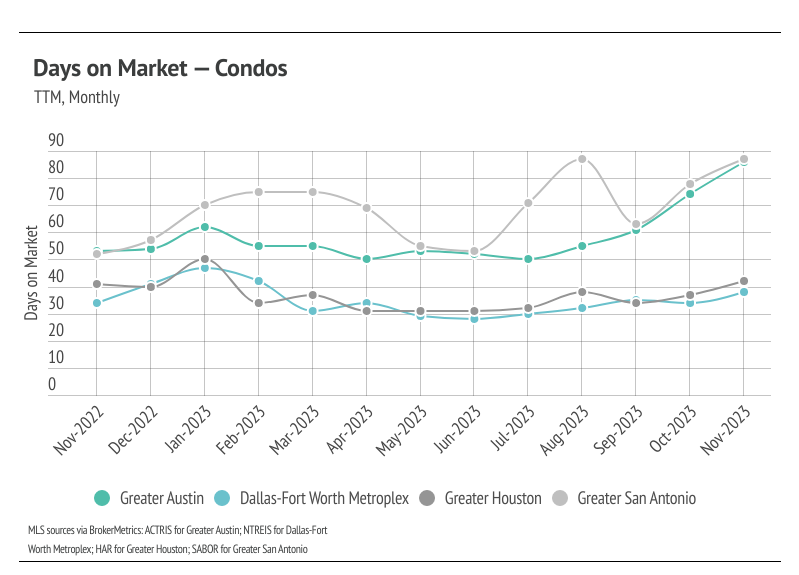

Inventory trended higher into the fall of 2023, which is far from the seasonal norm. Typically, inventory peaks in July or August and declines through December or January. In November, as sales and new listings declined, inventory fell from October to November. Notably, inventory reached a two-year high in October for single-family homes in Greater Houston and Greater San Antonio, and for condos in Greater Houston, before dropping slightly in November. Supply in Texas is rare in the United States, in that it actually built up to pre-pandemic levels this year, moving higher primarily due to softening demand caused by higher interest rates and normal seasonality. New listings have been slightly lower than last year, so inventory growth has been driven by fewer sales.

As demand slows, buyers are gaining slightly more negotiating power and paying less than asking price on average. The average seller is receiving a lower percentage of list price than they did in the first half of the year, but only by 2-3%. The market will likely be slower during the holiday season, but buyer competition will ramp up meaningfully in the spring, which will create price support.

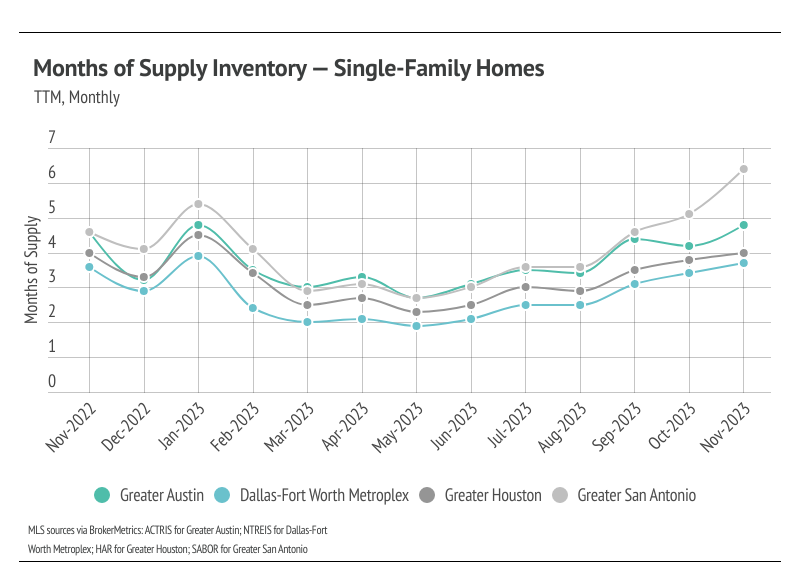

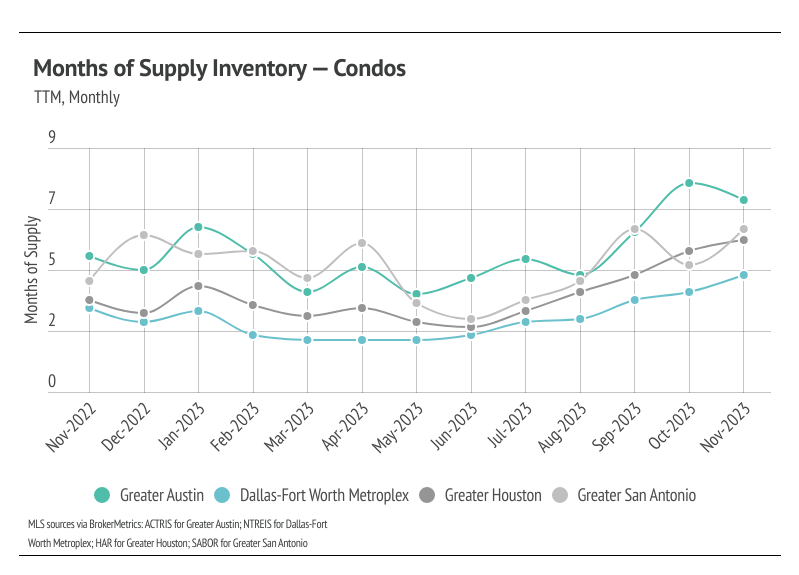

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around four to five months in Texas, which indicates a balanced market. An MSI lower than four indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while an MSI higher than five indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI rose significantly over the past five months largely due to the decline in sales and longer time on the market. Currently, for single-family homes, MSI indicates that Greater San Antonio favors buyers, Greater Austin and Greater Houston are balanced, and Dallas-Fort Worth still favors sellers. For condos, MSI indicates that the markets favor buyers except for Dallas-Fort Worth, which is balanced.

Stay up to date on the latest real estate trends.

May 2026

April 2026

March 2026

February 2026

January 2026

Trusted Experts in the Palisades, Santa Monica, and Brentwood Real Estate Markets

How Sellers In Pacific Palisades, Santa Monica And Brentwood Get It Right

December 2025

November 2025

You’ve got questions and we can’t wait to answer them.