Market Update Dallas

Note: You can find the charts & graphs for the Big Story at the end of the following section.

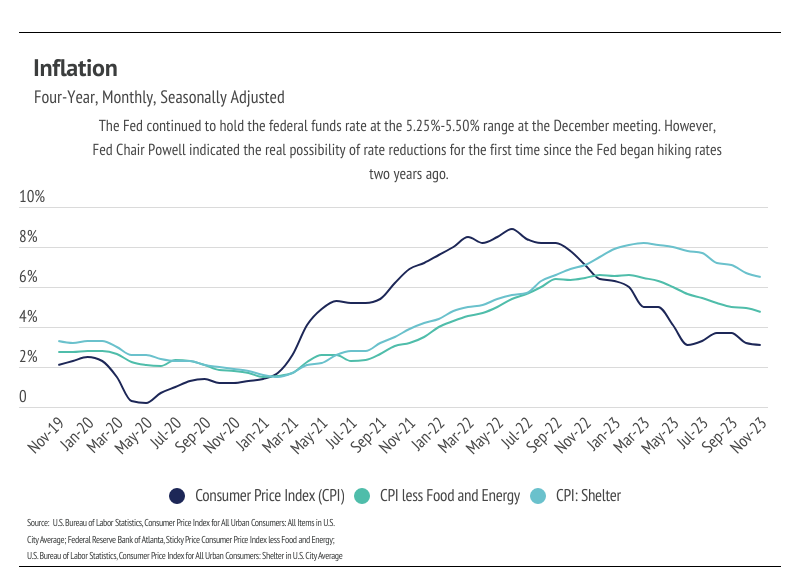

The next Fed meeting isn’t until the end of January, but financial markets have already made major assumptions about what the Fed will do in 2024. In the December 2023 meeting, Fed members indicated there would likely be three 0.25% cuts to the fed funds rate by the end of 2024, but they noted a high degree of uncertainty. Markets took this news and made their own conclusions. As of January 3, 2024, fed funds futures traders (the people who make a lot of money being right about where rates will go) expect the Fed to cut the federal funds rate by a quarter point six times in 2024. Currently, the fed funds rate is between 5.25% and 5.50%.

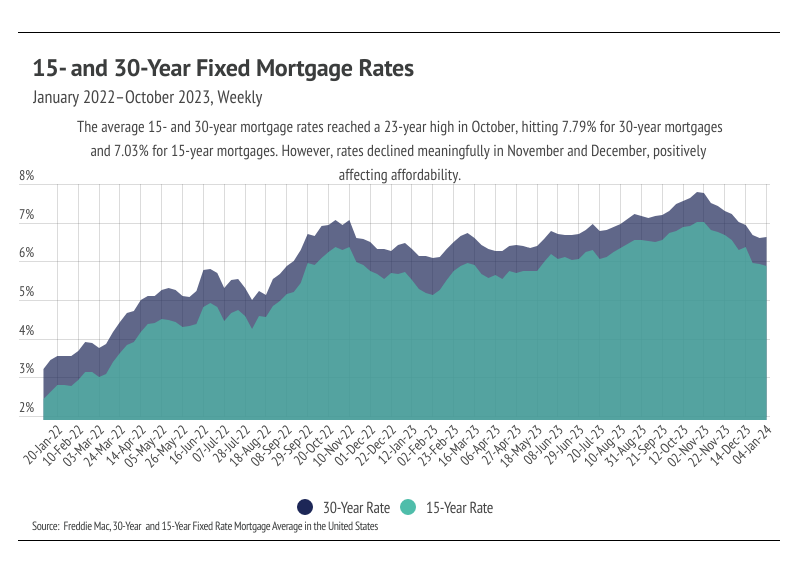

In any case, for the >70% of homebuyers who finance their purchases with mortgages, rate cuts are very good news, as shown by the month-over-month increase in sales. However, even before the December meeting, economic indicators seemed favorable for rate cuts, which, in part, caused mortgage rates to drop 0.57% in November 2023 — a significant fall from the 23-year high of 7.79% in October. Markets move a lot faster than the Fed, and the 1.18% mortgage rate drop in November and December brings to mind the trends we saw in the first quarter of 2022. In December 2021, Fed Chair Jerome Powell stated that they were increasing rates beginning in March 2022, but mortgage rates increased by about a point in the first quarter even before the Fed made any changes.

The 1.18% decline in mortgage rates has set the stage for a much busier spring and summer season, although we still expect a relatively slow first quarter. Interest rates are still too high for potential buyers and sellers to rush back to the market, especially when they expect further rate cuts. However, if mortgage rates were to drop another point to around 5.5%, a huge number of participants would jump back into the market. Remember that every 1% decrease in interest rates roughly equates to a 10% decrease in monthly financing costs. The inverse is also true, which is why rates have priced buyers out of the market and remain the primary cause of the market slowdown over the past two years.

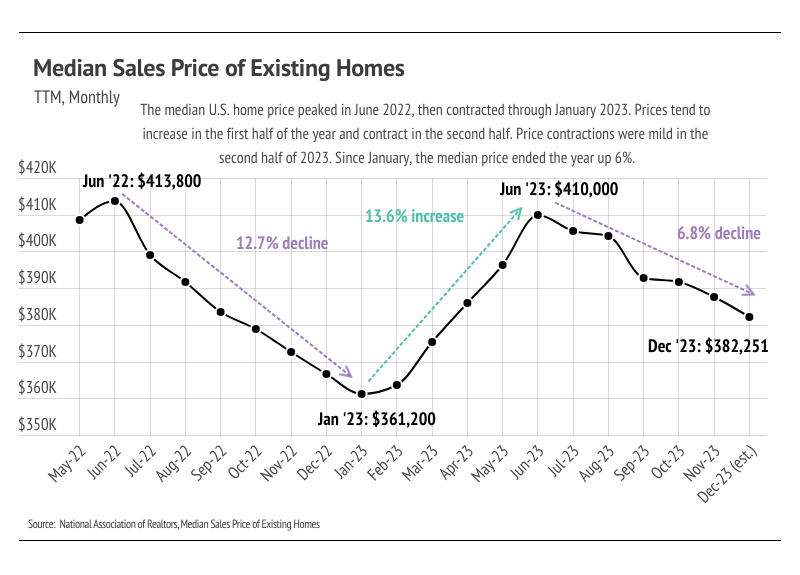

Because inventory hasn’t grown, prices haven’t meaningfully declined. In fact, home prices currently fall only 8% below the June 2022 all-time high, which means that any savings will likely come from rate drops. Even if a significant number of sellers come to market, there’s enough pent-up demand that inventory won’t be able to grow enough for prices to stagnate or decline outside of normal seasonal trends. On top of that, home prices almost always appreciate. In other words, betting on home prices to decline is statistically similar to betting on 00 in roulette. Nationally, the median price will likely hit a new all-time high in June 2024. The National Association of Realtors’ Chief Economist Lawrence Yun recently remarked that home prices keep marching higher, and only a dramatic rise in supply will dampen price appreciation.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. In general, higher-priced regions (the West and Northeast) have been hit harder by mortgage rate hikes than less expensive markets (the South and Midwest) because of the absolute dollar cost of the rate hikes and limited ability to build new homes. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

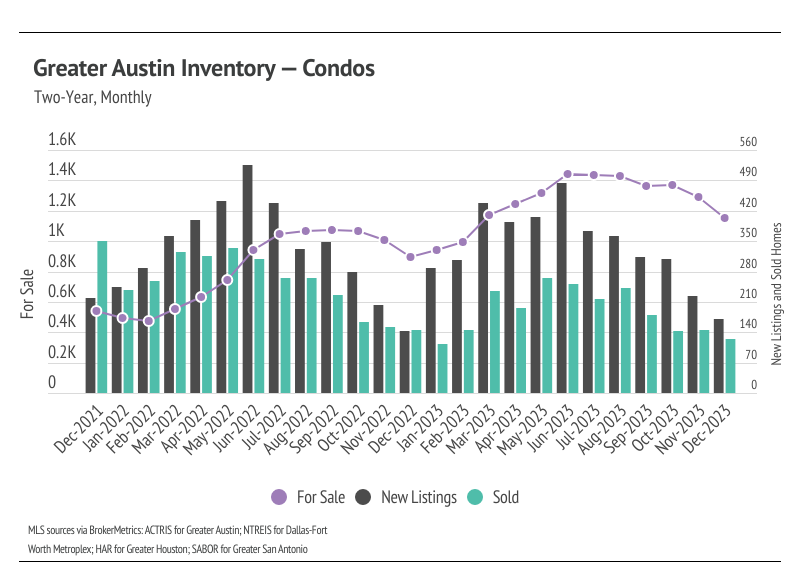

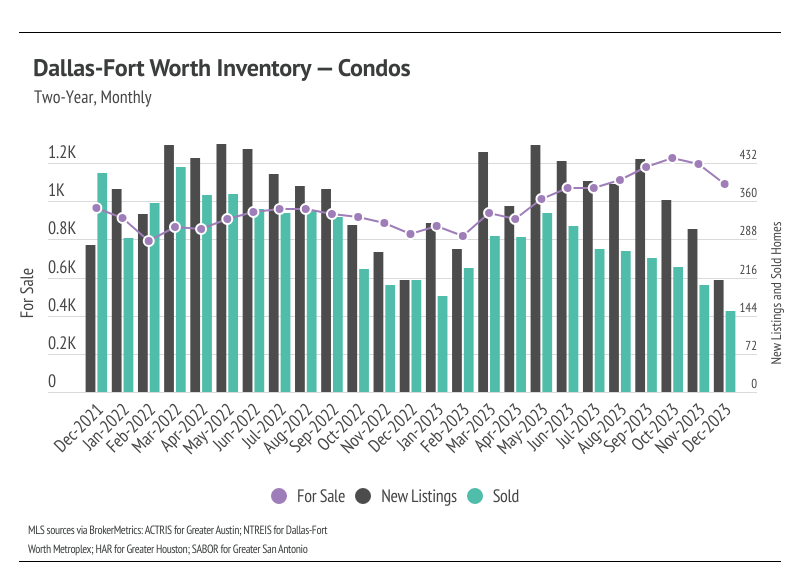

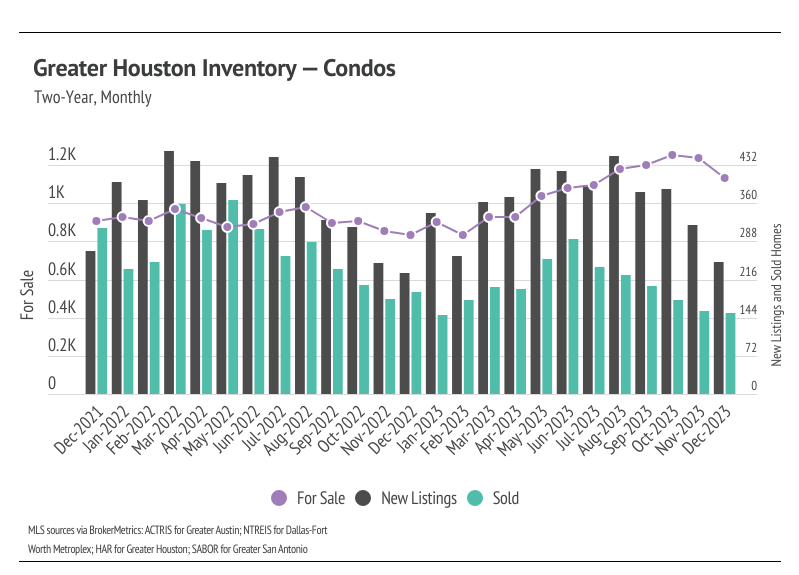

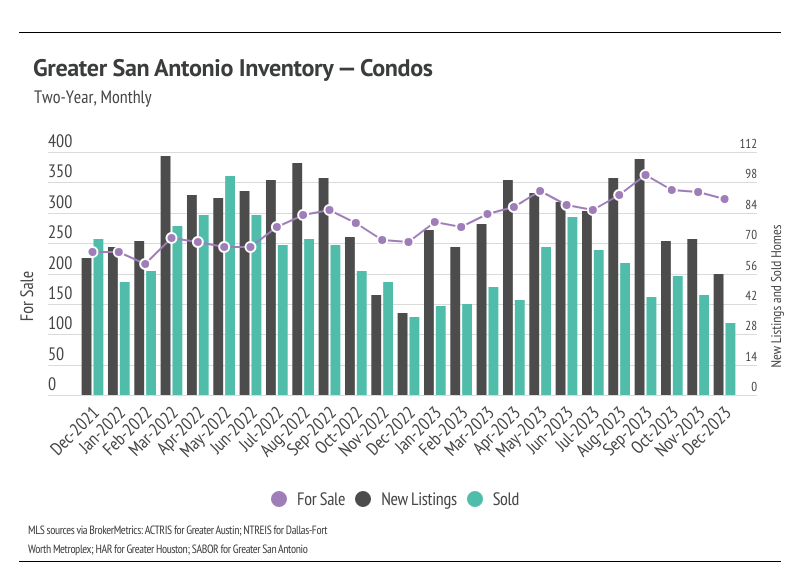

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

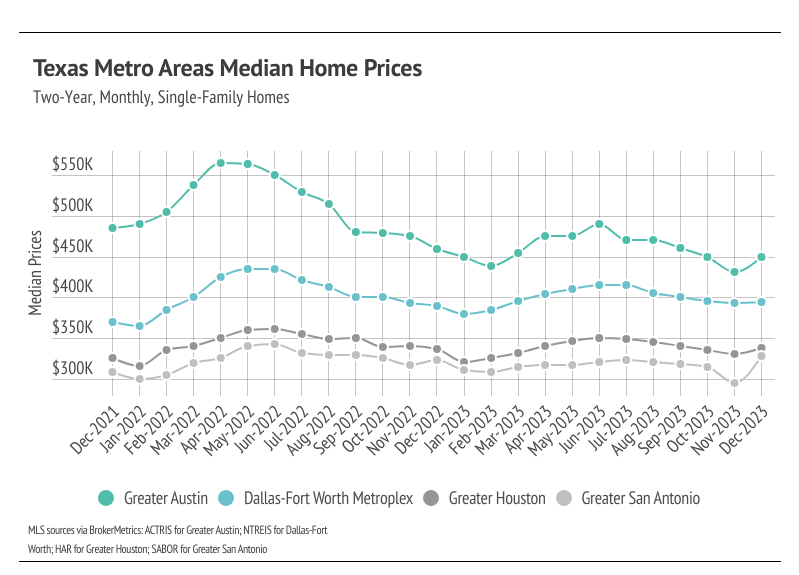

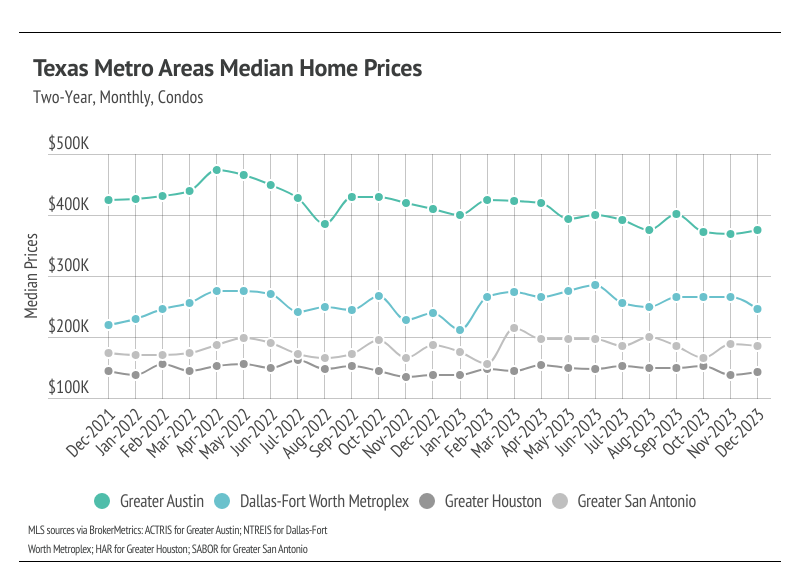

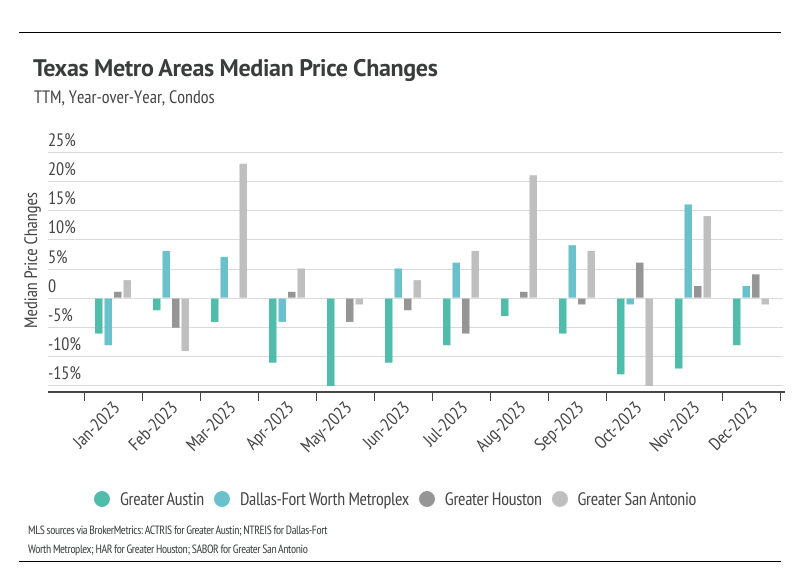

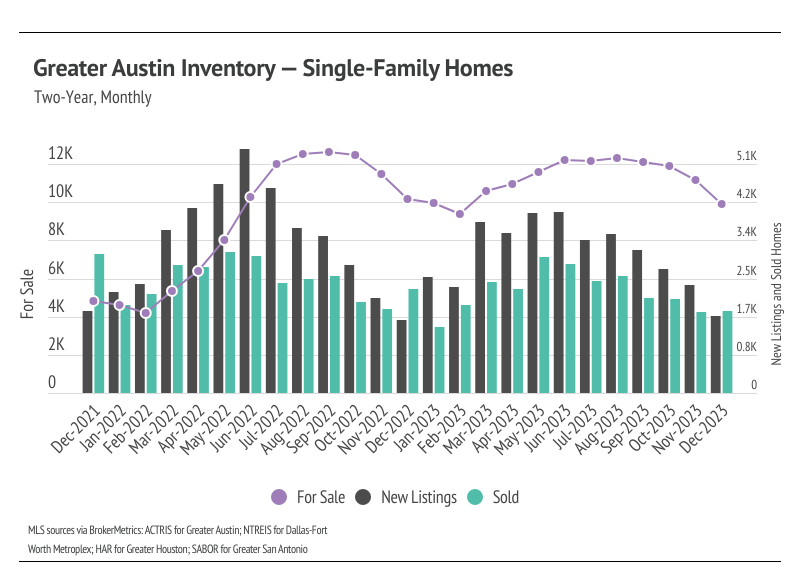

In Texas, the home prices haven’t been largely affected by rising mortgage rates with the exception of Greater Austin, which has had a major price contraction since May 2022. Broadly, price contractions are normal in the second half of the year, so it’s hard to conclude that higher rates have had any meaningful effect on price across most of Texas’s major metros. We expect prices to remain below peak in the winter months, but as interest rates decline, prices will almost certainly reach new highs in the first half of 2024 in all the selected major markets except Greater Austin. Additionally, the inventory build-up in 2023 will create a healthier market in 2024, satiating demand as it grows.

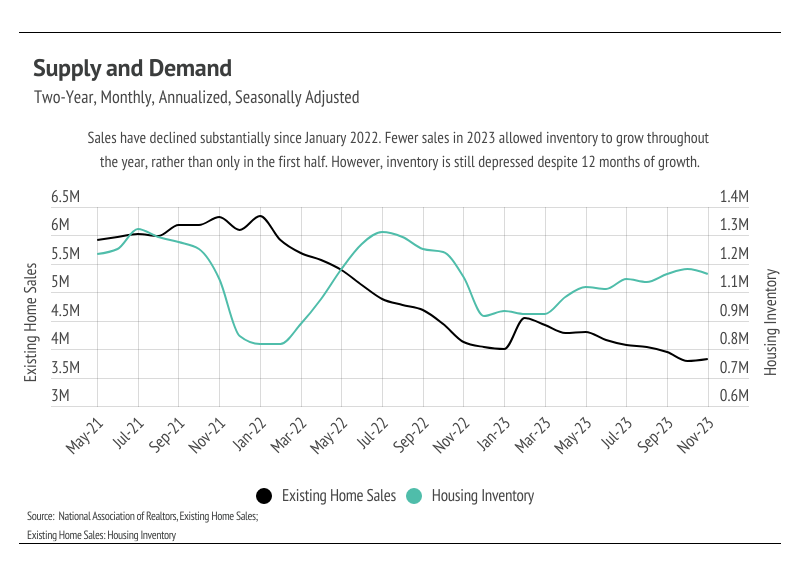

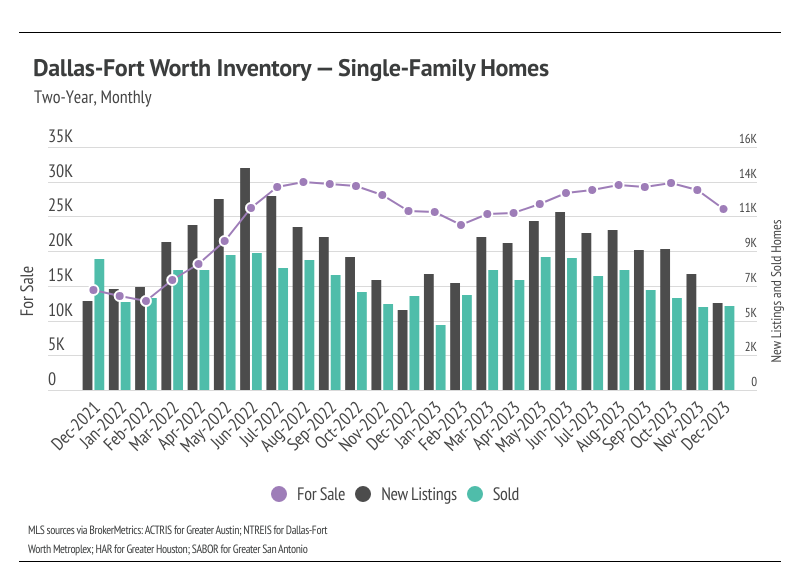

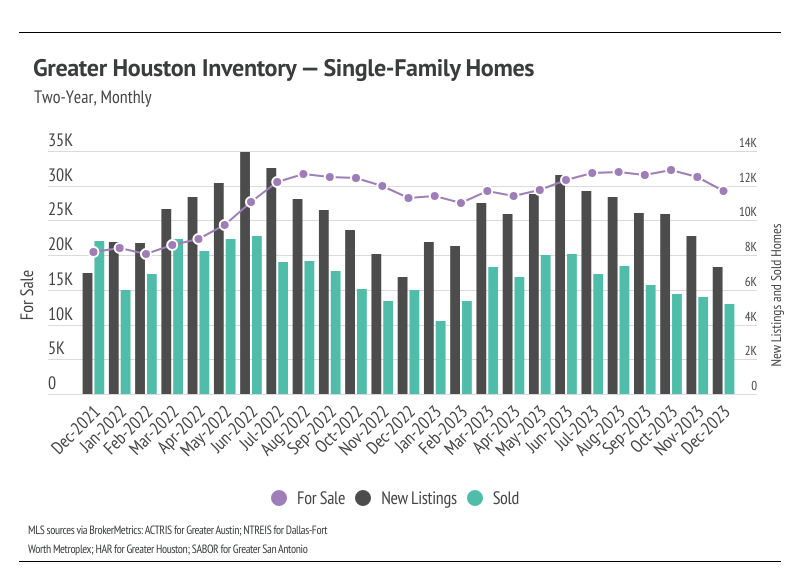

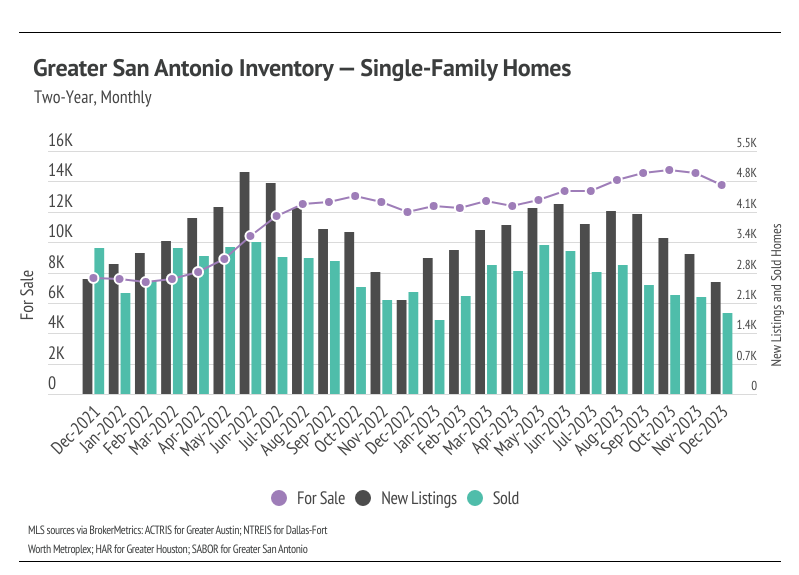

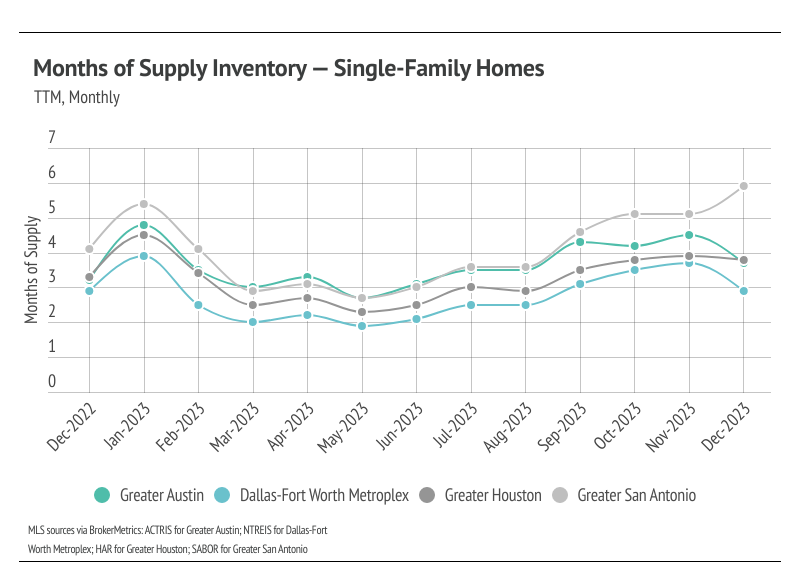

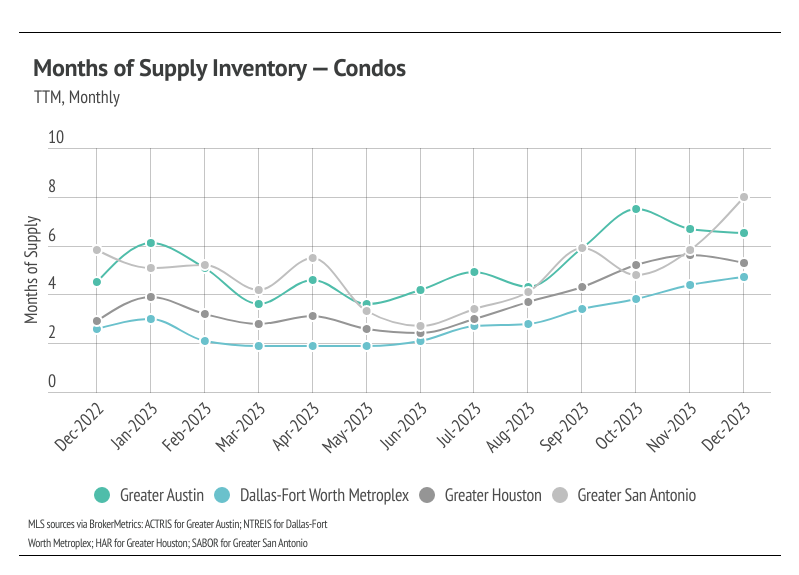

High mortgage rates soften both supply and demand, so ideally, as rates fall, far more sellers will come to the market. Rising demand can only do so much for the market if there isn’t supply to meet it. Unlike 2023 inventory, 2024 inventory has a much better chance of following more typical seasonal patterns.

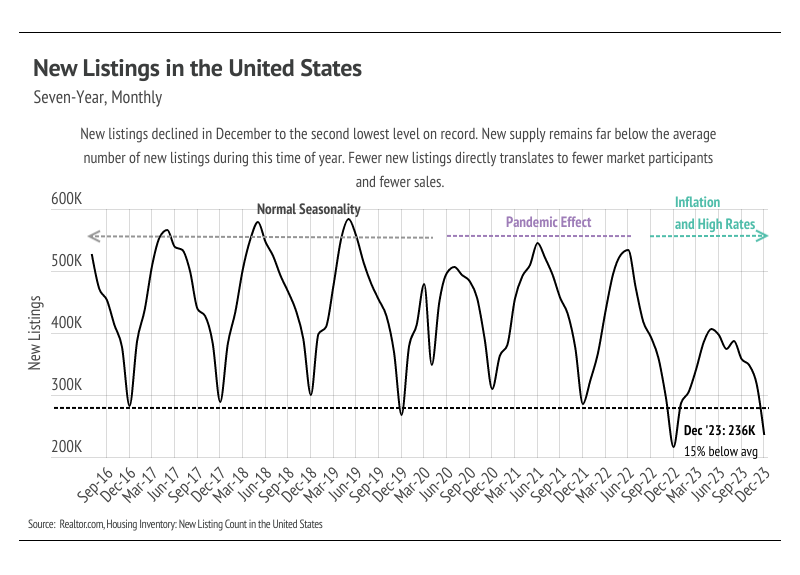

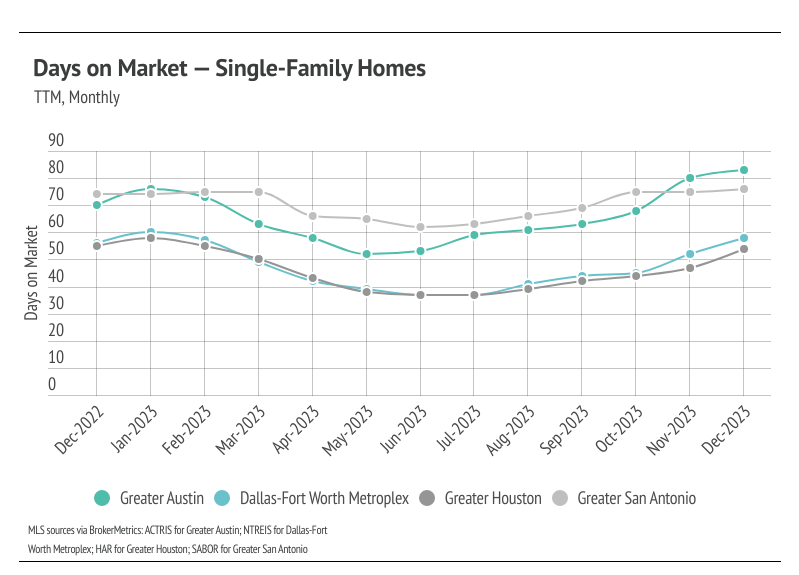

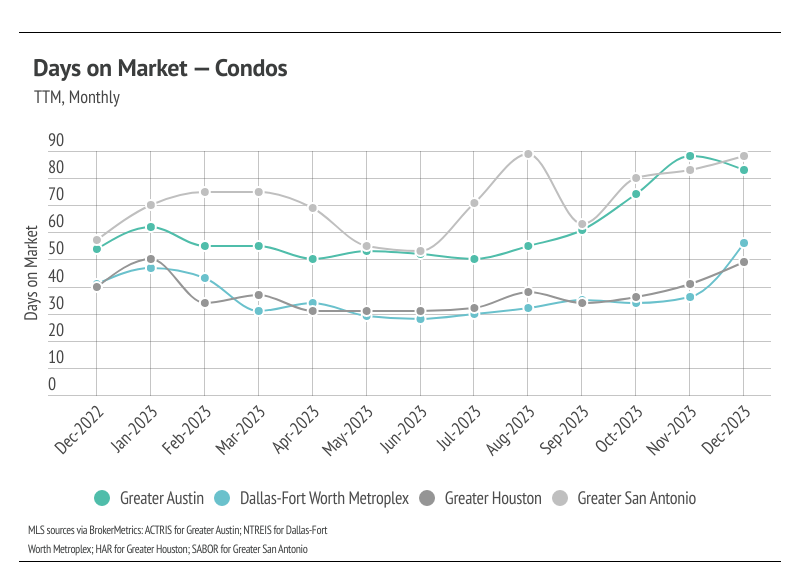

Inventory trended higher into the fall of 2023, which is far from the seasonal norm. Typically, inventory peaks in July or August and declines through December or January. In November and December, as sales and new listings declined, inventory fell from the October 2023 peaks. Notably, inventory reached a two-year high in October for single-family homes in Greater Houston and Greater San Antonio, and for condos in Greater Houston, before dropping in November and December. Inventory levels in Texas are unusual in the United States, in that they actually built up to pre-pandemic levels in 2023, moving higher primarily due to softening demand caused by higher interest rates and normal seasonality. New listings have been slightly lower than last year, so inventory growth has been driven by fewer sales.

As demand slows, buyers are gaining slightly more negotiating power and paying less than asking price on average. The average seller is receiving a lower percentage of list price than they did in the first half of the year, but only by 2-3%. The market generally slows considerably during the holiday season, but buyer competition will ramp up meaningfully in the spring, which will create price support.

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around four to five months in Texas, which indicates a balanced market. An MSI lower than four indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while an MSI higher than five indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI rose significantly over the past six months largely due to the decline in sales and longer time on the market. Currently, for single-family homes, MSI indicates that Greater San Antonio favors buyers, while Greater Austin, Dallas-Fort Worth, and Greater Houston favor sellers. For condos, MSI indicates that the markets favor buyers except for Dallas-Fort Worth, which is balanced.

Stay up to date on the latest real estate trends.

April 2026

March 2026

February 2026

January 2026

Trusted Experts in the Palisades, Santa Monica, and Brentwood Real Estate Markets

How Sellers In Pacific Palisades, Santa Monica And Brentwood Get It Right

December 2025

November 2025

October 2025

You’ve got questions and we can’t wait to answer them.